What Your Financial Advisor Isn't Telling You About Retirement Fees (Industry Insider Reveals All)

After 15 years in the financial services industry, I’m about to break the code of silence.

The retirement planning industry has a dirty secret: the fees you’re paying are often 2-3 times higher than what you’re told, and these hidden costs are quietly stealing hundreds of thousands of dollars from your retirement.

Most financial advisors won’t discuss this because they’re profiting from your ignorance. But after watching too many hardworking people get financially abused by the system that’s supposed to help them, I can’t stay quiet anymore.

Here’s everything the industry doesn’t want you to know about retirement fees.

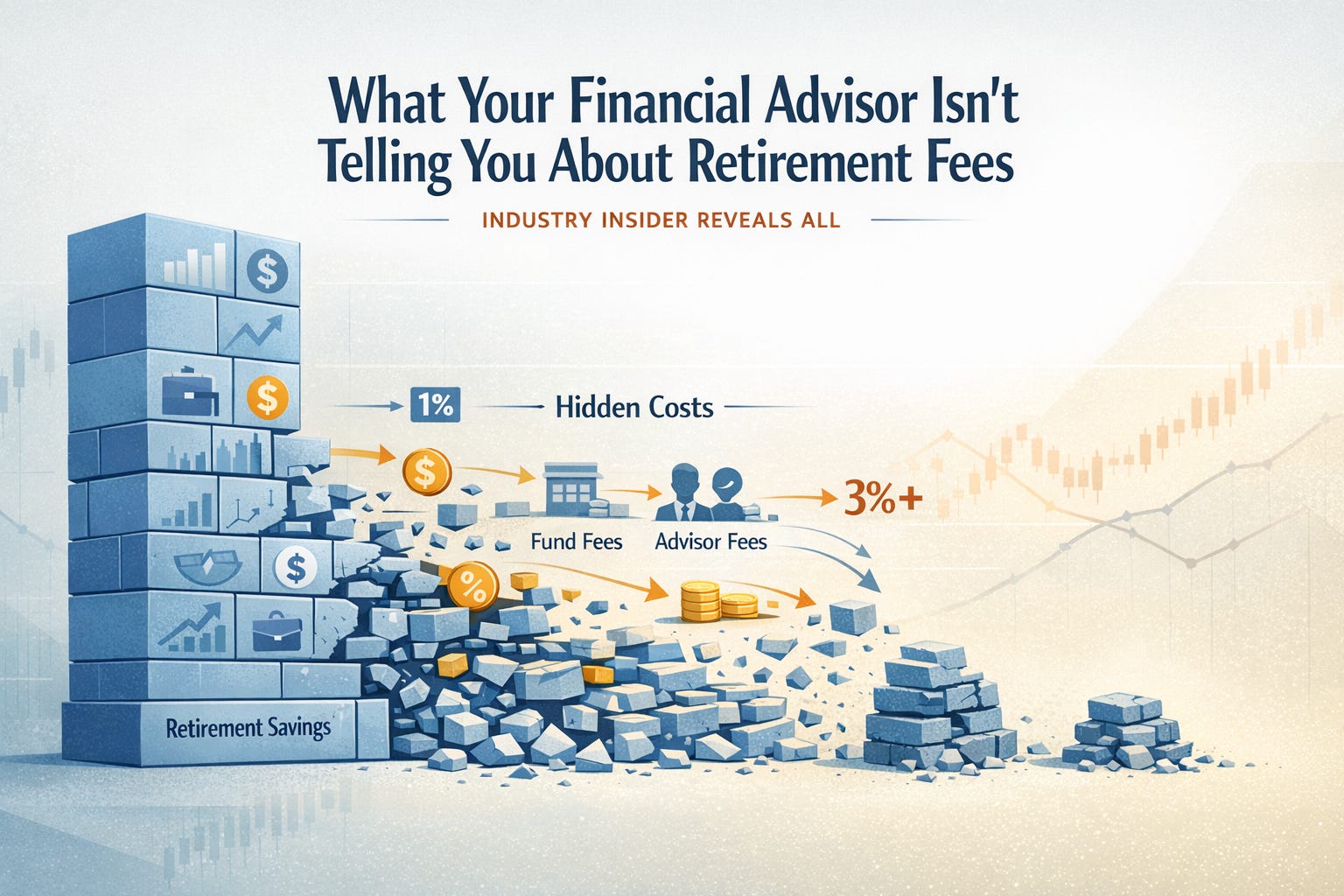

The Fee Iceberg: What You See vs. What You Pay

What most people think they’re paying: “My advisor charges 1% per year.”

What they’re actually paying: Often 2.5% to 4% annually when you add up all the hidden layers. On a $500,000 portfolio, that’s the difference between $5,000 and $20,000 per year in fees.

Over 20 years, this difference costs you approximately $300,000 in lost retirement wealth – money that should be working for you, not padding advisor profits.

Layer 1: The Advisor Fee (What They Tell You About)

This is the only fee most advisors clearly disclose:

● Investment advisory fee: Typically 1% to 1.5% of assets annually

● Financial planning fee: Sometimes included, sometimes extra ($2,000-$10,000)

Red flag: If your advisor can’t clearly explain their fee structure in under 30 seconds, you’re probably being overcharged.

Layer 2: Investment Product Fees (The Silent Wealth Killer)

Mutual fund expense ratios: The annual fee charged by mutual funds

● Actively managed funds: Often 0.75% to 1.5% annually

● Index funds: Typically 0.03% to 0.20% annually

● Specialty funds: Can exceed 2% annually

Real example: Your advisor puts you in American Funds Growth Fund of America (expense ratio: 0.66%) instead of Vanguard Total Stock Market Index (expense ratio: 0.03%). On $100,000, that’s $630 vs. $30 annually – a $600 difference for virtually identical market exposure.

Why this happens: Many advisors receive kickbacks (called “12b-1 fees”) from expensive mutual fund companies. They make more money when you own expensive funds.

Layer 3: Platform and Custodial Fees (The Hidden Charges)

Custodial fees: Where your investments are held

● Annual account fees: $50-$200 per account

● Transaction fees: $10-$50 per trade

● Inactivity fees: Charges if you don’t trade enough

● Transfer fees: $50-$100 to move accounts

Platform fees: Additional charges from investment platforms

● Wrap fees: 0.25% to 0.50% annually for “platform access”

● Administrative fees: 0.10% to 0.25% for record-keeping

● Technology fees: $50-$200 annually for online access

Layer 4: Insurance Product Commissions (The Profit Goldmine)

Variable annuities: Often the most profitable products for advisors

● Annual fees: 2% to 4% of your investment

● Surrender charges: 7% to 10% if you exit early

● Rider fees: Additional 0.5% to 1.5% for “benefits”

● Investment options: Often limited to expensive sub-accounts

Whole life insurance: Marketed as “investments” but actually insurance

● First-year commission: Often 50% to 100% of your premium

● Annual fees: 1% to 3% of cash value

● Hidden costs: Mortality charges, administrative fees, policy loans

Real shocker: An advisor selling you a $100,000 variable annuity might earn $7,000 in upfront commission plus $2,000-$4,000 annually in ongoing fees.

Layer 5: Transaction and Trading Costs (Death by a Thousand Cuts)

Bid-ask spreads: The difference between buying and selling prices

● Individual stocks: Usually minimal

● Bonds: Can be 0.5% to 2% per transaction

● Complex products: Sometimes 3% to 5%

Excessive trading: Churning that generates fees

● Turnover costs: Buying and selling generates transaction fees

● Tax consequences: Unnecessary capital gains taxes

● Market impact: Large trades can move prices against you

The 401(k) Fee Scandal Most People Don’t Know About

Your 401(k) probably has higher fees than your advisor’s personal investment account. Typical 401(k) fee structure:

● Plan administration fees: 0.50% to 1.50% annually

● Investment management fees: 0.50% to 2.00% per fund

● Individual service fees: $25-$100 per transaction

● Revenue sharing: Hidden kickbacks to plan providers

Total cost: Often 2% to 3% annually – double what you’d pay with optimal investment choices.

The kicker: Many employers don’t even know these fees exist because they’re buried in fund expense ratios and revenue-sharing agreements.

How Fee Layers Compound to Destroy Wealth

Example: $300,000 retirement account over 20 years

High-fee scenario (3% total annual fees):

● Ending balance: $456,000

● Total fees paid: $244,000

Low-fee scenario (0.5% total annual fees):

● Ending balance: $636,000

● Total fees paid: $80,000

The difference: $180,000 less retirement wealth plus $164,000 more in fees = $344,000 total impact That’s potentially 1-2 additional years of retirement income lost to excessive fees. The Commission vs. Fee-Only Deception

Commission-based advisors claim to provide “free” advice while earning money from product sales. The reality:

● Nothing is free – you pay through higher product costs

● Conflicts of interest are built into every recommendation

● Churning and product switching generates more commissions

● Your interests are secondary to advisor profits

Fee-only advisors charge transparent fees and don’t sell products.

The advantage:

● Aligned interests – they succeed when you succeed

● No hidden product commissions or kickbacks

● Recommendations based on what’s best for you

● Transparent fee structure

Red Flags: Signs You’re Being Fee-Abused

Your advisor exhibits these behaviors:

● Can’t clearly explain all fees you’re paying

● Recommends complex products you don’t understand

● Frequently suggests moving money between investments

● Pushes variable annuities or whole life insurance as “investments”

● Your investment returns consistently lag simple index funds

● You receive free dinners, gifts, or entertainment

Your statements show:

● Multiple layers of fees and charges

● High expense ratios (above 1% for most funds)

● Frequent trading and transaction fees

● Products with surrender charges or penalties

● Performance that doesn’t justify the costs

The Fee Negotiation Playbook

Most fees are negotiable, but advisors won’t volunteer this information. For advisory fees:

● $500,000-$1M: Often negotiable down to 0.75%

● $1M+: Should be 0.50% to 0.75%

● $5M+: Often 0.25% to 0.50%

For investment products:

● Institutional share classes: Lower fees for larger accounts

● Fee waivers: Sometimes available for loyalty or account size

● Platform negotiations: Custodial fees often waivable

The key: You have to ask. Advisors rarely offer fee reductions voluntarily.

Building a Low-Fee Retirement Strategy

Step 1: Audit your current fees

● Request fee disclosure from all providers

● Calculate total annual cost as percentage of assets

● Identify the highest-cost components

Step 2: Optimize investment selection

● Index funds over active funds when appropriate

● ETFs over mutual funds for tax efficiency

● Direct ownership over fund-of-funds to eliminate double fees

Step 3: Minimize platform costs

● Consolidate accounts to reduce custodial fees

● Choose low-cost custodians like Fidelity, Schwab, or Vanguard

● Negotiate or eliminate unnecessary platform fees

Step 4: Evaluate advisor value

● Does their value exceed their cost?

● Can you achieve similar results with lower fees?

● Are they providing comprehensive financial planning or just investment management? When Higher Fees Are Actually Worth It

Not all fees are bad. Sometimes paying more makes sense:

Comprehensive financial planning that addresses taxes, estate planning, insurance, and retirement income optimization can easily save more than it costs.

Specialized expertise in areas like business succession planning, tax optimization, or complex estate planning can provide enormous value.

Behavioral coaching that prevents emotional investment mistakes during market volatility often pays for itself many times over.

The key: The value provided must clearly exceed the fees charged.

The RetireNova Fee Philosophy

We believe in radical fee transparency because your money should work for you, not us. Our approach:

● Clear, disclosed fees with no hidden charges or conflicts

● Fee-only structure with no product commissions or kickbacks

● Institutional-quality investments at individual investor prices

● Comprehensive planning that often saves more in taxes than our fees cost

We’re successful when you’re successful – not when we sell you expensive products. Your Next Steps: Taking Control of Your Fees

The retirement fee game is rigged against you, but you don’t have to play by their rules. Every dollar you save in fees is a dollar that compounds for your benefit over decades.

Immediate actions you can take:

1. Request a complete fee analysis from your current providers

2. Calculate your total annual costs as a percentage of assets

3. Research low-cost alternatives for your largest holdings

4. Question every fee on your statements

5. Negotiate or eliminate unnecessary charges

At RetireNova, we provide complimentary fee analysis that typically identifies $5,000-$25,000 in annual fee savings for our clients.

We’ll show you:

● Exactly what you’re currently paying in all fee layers

● How these costs impact your long-term retirement wealth

● Specific strategies to reduce fees without sacrificing quality

● The real value you should expect for the fees you pay

Ready to stop letting hidden fees steal your retirement?

[Get Your Complimentary Fee Analysis]

Because every fee dollar you save is a retirement dollar you keep.