A 457(b) plan offers valuable retirement savings opportunities for state, local government, and certain non-profit employees. While its primary goal is long-term retirement security, life doesn’t always go according to plan. Situations may arise where participants need urgent access to funds. That’s where unforeseeable emergency distributions come in.

In this guide, we’ll explain:

What counts as an unforeseeable emergency under IRS rules

When these distributions can be used

The process through providers like T. Rowe Price

Tax consequences and planning considerations

Alternatives to consider before tapping into retirement savings

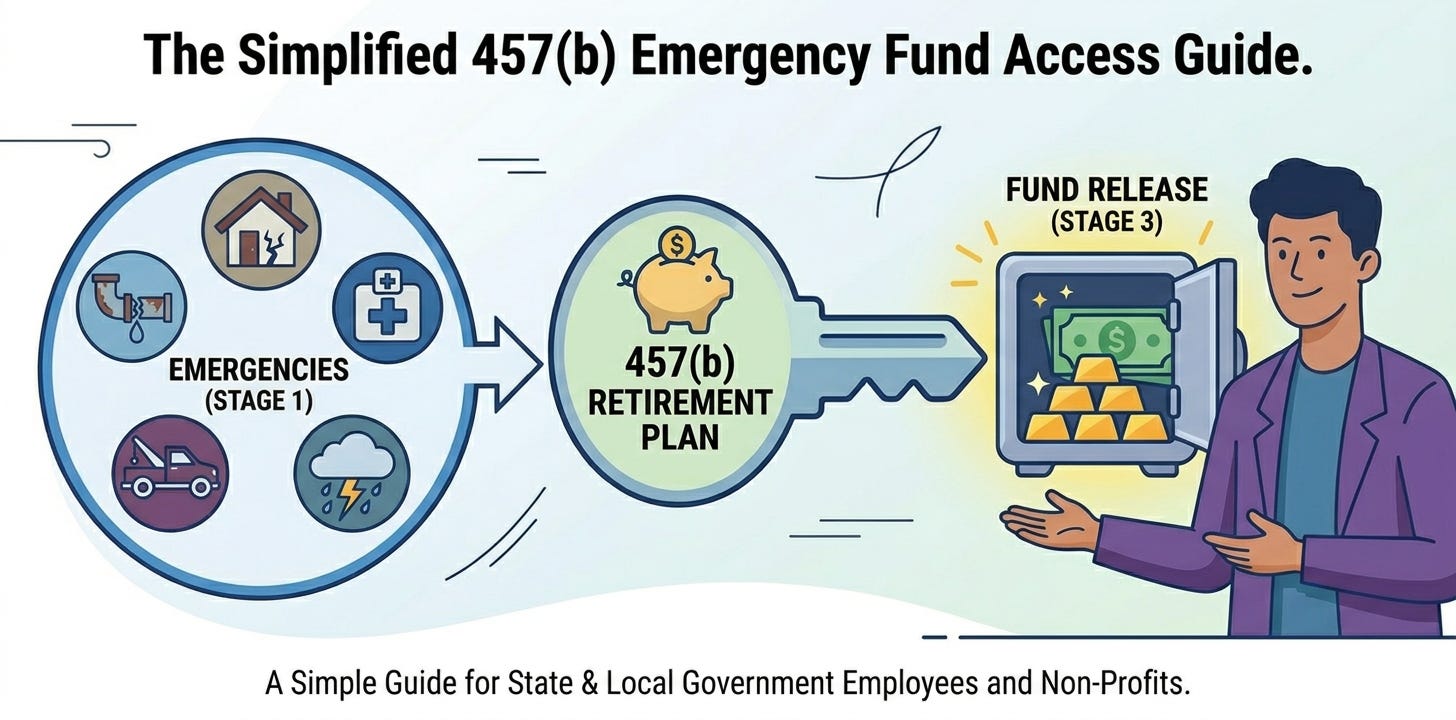

Defining an Unforeseeable Emergency

According to the IRS, an unforeseeable emergency distribution is a withdrawal from a 457(b) plan allowed when a participant faces a severe financial hardship resulting from:

An illness or accident of the participant, their spouse, or dependents

Loss of property due to casualty (e.g., fire, natural disaster)

Funeral expenses for a family member

Other extraordinary and unforeseeable circumstances arising from events beyond the participant’s control

The key phrase is “beyond the participant’s control.” Routine expenses such as buying a home, paying college tuition, or elective medical procedures are specifically excluded.

When Can They Be Used?

Only After All Other Resources Are Depleted

To qualify, you must show that the hardship cannot be relieved through insurance, liquidation of assets, or other resources. For example, if you could reasonably pay the expense using savings, a loan, or an insurance claim, the 457(b) plan will not approve the request.

Strict Plan Administrator Review

Each plan provider, such as T. Rowe Price, has a process for reviewing requests. Participants must submit documentation hospital bills, insurance denials, repair estimates, etc.to prove the emergency qualifies.

Limited to Actual Need

Distributions are limited to the amount necessary to satisfy the emergency, plus taxes. You cannot withdraw more than what the hardship requires.

Examples of Qualifying Situations

Medical Emergency: A sudden accident leading to uncovered hospital costs.

Natural Disaster: Home destroyed by a tornado, with costs exceeding insurance coverage.

Funeral Expenses: Unexpected death of a spouse or dependent requiring immediate funds.

Extraordinary Expenses: Court-ordered payments or similar rare events not caused by personal choice.

By contrast, college tuition, credit card bills, or buying a new car do not qualify.

How Providers Like T. Rowe Price Handle Requests

T. Rowe Price and similar custodians follow IRS rules closely:

Application Process – Participants file a hardship withdrawal request form.

Supporting Evidence – Bills, receipts, or insurance letters must accompany the request.

Administrator Review – T. Rowe Price, as plan administrator, determines if the request meets IRS “unforeseeable emergency” standards.

Distribution Approval – If approved, funds are distributed directly to the participant. This strict review ensures withdrawals are truly for emergencies and keeps the plan compliant.

Tax Treatment of Emergency Distributions

Subject to Income Tax – All distributions are taxable as ordinary income in the year received.

No 10% Early Withdrawal Penalty – Unlike 401(k)s or IRAs, 457(b) plans do not impose a 10% penalty on early withdrawals, even for emergencies. This unique feature makes 457(b) plans more flexible in crisis situations.

State Taxes Apply – Depending on your residency, state income tax may also apply unless your state exempts retirement income.

Pros and Cons of Using Emergency Distributions

Benefits

Immediate access to funds when no other options are available

Avoidance of early withdrawal penalties (unlike many other retirement accounts)

Provides a safety net for severe hardships

Drawbacks

Reduces long-term retirement savings and growth

Taxable as income in the year of withdrawal

Requires strict documentation and approval, which can delay access

Alternatives to Consider

Before applying for an emergency distribution, explore alternatives such as:

Insurance claims – Ensure policies are fully utilized.

Emergency savings – Designed for exactly these situations.

Plan loans (if allowed) – Some 457(b) plans permit participant loans, which may be repaid to restore savings.

Other financial aid – Government disaster relief programs or charitable support. Using these options may protect your retirement balance and avoid long-term consequences.

Key Planning Considerations

Use only as a last resort. Emergency distributions are designed for severe, unpredictable hardships.

Document everything. Approval depends on strong evidence of need.

Consider timing. Large distributions can push you into a higher tax bracket.

Rebuild savings. After an emergency withdrawal, aim to replenish retirement contributions as soon as possible.

About Nova Wealth

At Nova Wealth, we focus on helping retirees and pre-retirees build predictable and sustainable income in retirement. Our approach centers on personalized strategies that deliver steady, reliable cash flow so you can enjoy your next chapter with confidence. We believe retirement should feel secure and stress free free from uncertainty and full of clarity.

Whether you are evaluating 457(b) rollover options, considering catch-up contributions, or planning for emergency distributions, Nova Wealth is here to guide you every step of the way. Contact us today to start building a retirement income plan designed to give you peace of mind for the years ahead.