Everyone wants to save for retirement, but few realise that how you save can make all the difference in what you keep.

That’s where the Traditional 401(k) and Roth 401(k) come in. Both accounts are designed to help you build long-term wealth, yet they take very different approaches to taxes. The key question isn’t which one is better, it’s when you want to pay taxes: now or later?

A Traditional 401(k) gives you an immediate tax break by reducing your taxable income today, while a Roth 401(k) lets your money grow tax-free for tomorrow. Choosing between them isn’t about guessing the market; it’s about understanding your tax situation, income goals, and what kind of retirement you want to fund.

Before we compare the two, let’s take a moment to understand what a 401(k) really is and why it’s such a powerful part of your retirement plan.

What Is a 401(k) and Why Does It Matter for Retirement Planning?

A 401(k) is one of the simplest and most effective ways to save for retirement. It’s an employer-sponsored savings plan that lets you automatically invest a portion of your paycheck into long-term investments, such as mutual funds or index funds.

The best part? Many employers offer matching contributions, essentially free money that helps you grow your savings faster. If your employer matches 50% of every dollar you contribute up to a certain limit, that’s an instant return on your investment before you even start earning market growth.

Beyond employer matches, the real advantage of a 401(k) lies in its tax benefits. Depending on whether you choose a Traditional or Roth 401(k), those tax advantages apply either today or later in retirement.

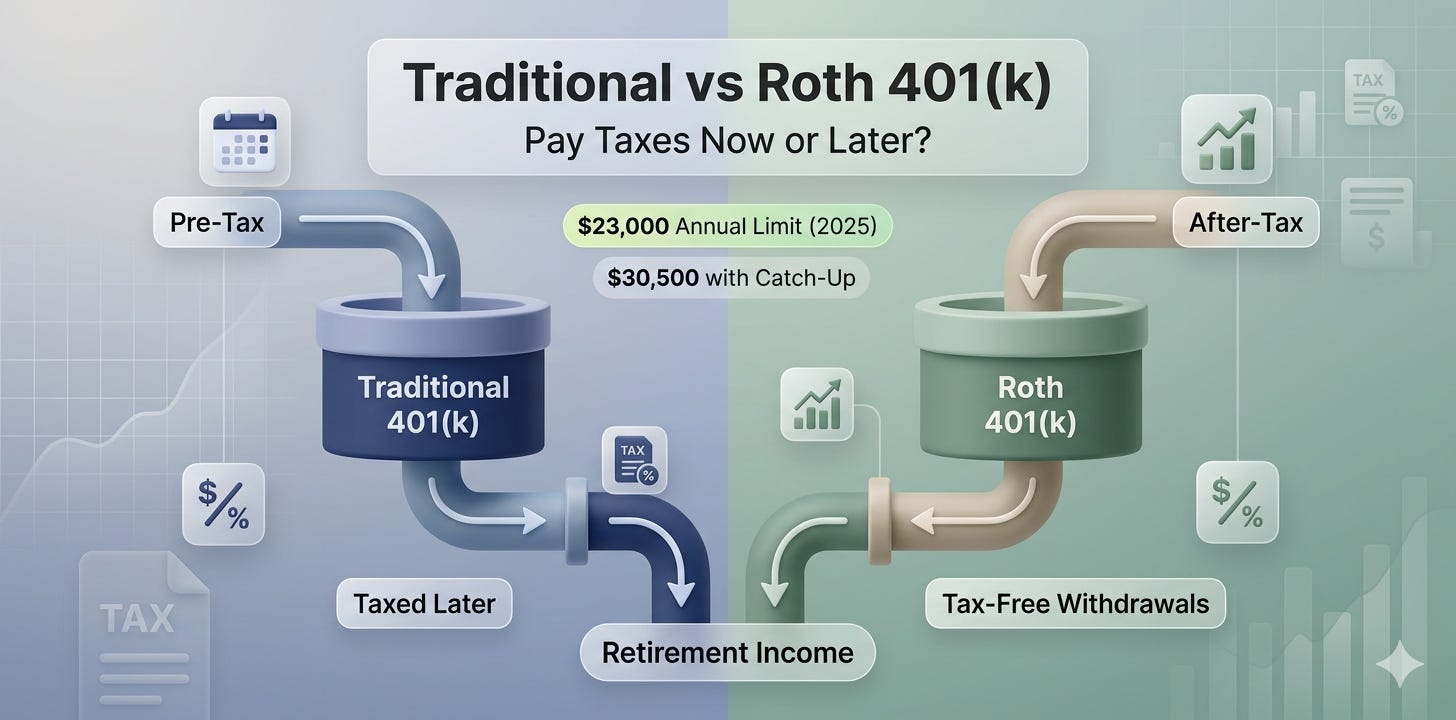

For 2025, the IRS allows you to contribute up to $23,000 per year, or $30,500 if you’re age 50 or older (thanks to a $7,500 catch-up contribution). These limits apply to both Traditional and Roth accounts combined, giving you flexibility to divide contributions as you see fit.

Understanding Traditional 401(k) Accounts

A Traditional 401(k) allows you to make contributions using pre-tax dollars. That means money goes into your account before income taxes are applied, reducing your taxable income for the year.

Let’s look at a simple example. Suppose you earn $70,000 a year and decide to contribute $10,000 to your Traditional 401(k). You’ll only be taxed on $60,000 of income, effectively saving on taxes right now.

Those contributions then grow tax-deferred until retirement. When you start withdrawing the funds, usually after age 59½, the money you take out is taxed as ordinary income. That’s why a Traditional 401(k) often works best for people who expect to be in a lower tax bracket after they retire.

It’s important to note that required minimum distributions (RMDs) begin at age 73, meaning you’ll need to start withdrawing a certain amount each year, even if you don’t need the income.

Understanding Roth 401(k) Accounts

The Roth 401(k) takes the same foundation as the Traditional plan, but flips when you pay taxes.

Instead of using pre-tax dollars, you contribute after-tax money, meaning you pay income tax on your contributions now, but your withdrawals in retirement are completely tax-free.

Here’s what that looks like in real life.

If you earn $70,000 and contribute $10,000 to a Roth 401(k), you’ll still be taxed on your full $70,000 income this year. But once that money is in your Roth account, it grows tax-free, and when you retire, both your contributions and your earnings can be withdrawn without paying another cent in taxes (as long as you meet the age and holding requirements).

Roth 401(k)s are especially attractive for younger workers or anyone who expects to be in a higher tax bracket in retirement. Paying taxes now, when rates are lower, can lead to major long-term savings later.

Key Points About Roth 401(k) Contribution Rules

● Funded with after-tax contributions.

● Follows the same annual limits as a Traditional 401(k).

● No income limits (unlike Roth IRAs).

● Tax-free withdrawals after age 59½, provided the account has been held for at least five years.

In short, a Roth 401(k) gives you tax freedom in retirement, turning today’s dollars into tomorrow’s untaxed income.

Before deciding which plan fits best, it helps to see how these two options compare side by side.

Traditional vs Roth 401k: Key Differences Explained So how do these accounts truly compare? Let’s break down the main distinctions.

Contributions

Traditional 401(k): Pre-tax (reduces your taxable income today)

Roth 401(k): After-tax (no immediate tax deduction)

Withdrawals

Traditional 401(k): Taxed as ordinary income in retirement

Roth 401(k): Tax-free in retirement

Contribution Limits (2025)

Traditional 401(k): $23,000 ($30,500 with catch-up contributions)

Roth 401(k): $23,000 ($30,500 with catch-up contributions)

Required Minimum Distributions (RMDs)

Traditional 401(k): Required starting at age 73

Roth 401(k): Required at age 73 (but distributions are tax-free)

Best For

Traditional 401(k): Those in a high tax bracket now, expecting lower taxes later

Roth 401(k): Younger earners or those expecting higher retirement tax rates

Tax Benefits and Retirement Income Planning

Taxes are at the heart of the Traditional vs Roth 401(k) decision. Both help you build wealth for retirement, but they just do it on different timelines.

A Traditional 401(k) gives you upfront tax relief. You lower your taxable income now, which can be a big benefit if you’re currently in a high tax bracket.

A Roth 401(k) provides back-end relief, meaning you pay taxes today but enjoy tax-free income later when you withdraw your savings.

Here’s how that might look in real scenarios:

● Traditional 401(k): Best for high earners today who expect a lower income in retirement.

● Roth 401(k): Best for younger professionals or anyone who expects higher taxes in the future.

Both options lead to the same goal, financial independence in retirement, but the path differs based on your current situation and future outlook.

Contribution Limits for 2025

Before deciding where to put your money, it helps to know how much you can actually contribute.

For 2025, the IRS has kept 401(k) limits generous:

● Annual contribution limit: $23,000 (for both Traditional and Roth 401(k)s combined)

● Catch-up contribution (age 50+): $7,500

● Total possible contribution: $30,500 for savers 50 and older

These limits apply no matter which version you choose.

If your employer offers both, you can split your contribution, for example, $11,500 into a Traditional 401(k) and $11,500 into a Roth 401(k) as long as the combined total doesn’t exceed $23,000.

The key is to maximize what you can, especially if your employer matches part of your contribution. Every matched dollar is free money that compounds over time.

Choosing Between Traditional and Roth 401(k)

Deciding between a Traditional and Roth 401(k) isn’t about picking a winner it’s about aligning your choice with your financial reality.

Here’s how to think through the decision:

1. Current vs Future Tax Bracket

If you’re in a high tax bracket today and expect lower taxes later, the Traditional 401(k) can reduce your taxable income now.

If you’re in a lower bracket today or expect taxes to rise, the Roth 401(k) may be smarter.

2. Age and Career Stage

Younger workers often lean toward Roth because they have decades for tax-free growth.

High-earning professionals nearing retirement may prefer a Traditional for immediate deductions.

3. Employer Match

Both plans qualify for matching, but your employer’s match always goes into a pre-tax (Traditional) account.

That’s okay, it simply means part of your savings will be taxed later.

4. Retirement Goals

Think about your ideal lifestyle. Will tax-free withdrawals give you more flexibility? Or does reducing today’s taxable income free up extra cash to invest elsewhere?

Many savers find a blend of both works best. Splitting contributions between Traditional and Roth accounts helps hedge against future tax changes.

DIY Checklist: Choose Between Traditional and Roth 401(k)

Use this step-by-step guide to evaluate your own situation.

1. Review Your Current Tax Bracket

High bracket? Traditional 401(k) can cut your taxable income today.

Lower bracket? Roth 401(k) may be smarter for tax-free withdrawals later.

2. Compare Future Income Expectations

Estimate your retirement income. If you expect higher taxes down the road, Roth

contributions offer long-term protection.

3. Check 2025 Contribution Limits

You can put away up to $23,000 ($30,500 if 50+).

Split funds between accounts if your employer allows both.

4. Leverage Employer Matching

Always contribute enough to earn your full match; it’s free money that accelerates your growth.

5. Reassess Annually

Income and goals change. Review your plan every year to ensure your contributions and tax strategy still align.

Retirement planning isn’t one-and-done; it’s a habit.

A small tweak each year can translate into thousands of dollars in future savings.

Final Thoughts on Traditional vs Roth 401(k)

When it comes to saving for retirement, the real question isn’t which plan is better, it’s when you want to pay taxes.

A Traditional 401(k) rewards you now with lower taxable income and bigger upfront savings. A Roth 401(k) rewards you later with tax-free withdrawals and peace of mind in retirement. Both accounts are powerful tools for building long-term wealth; the right choice depends on your current income, future goals, and outlook on taxes.

Understanding the rules and limits is the first step. The next step is matching those details to your financial strategy.

At RetireNova, our advisors help you analyse how each option fits into your overall plan, from contribution strategy to long-term tax projections. Whether you prefer the immediate savings of a Traditional 401(k) or the future freedom of a Roth 401(k), we’ll help you find the balance that keeps your retirement on track.

FAQs

General 401(k) FAQs

1. What is the main difference between a Traditional and Roth 401(k)?

A Traditional 401(k) uses pre-tax contributions and taxes withdrawals later. A Roth 401(k) uses after-tax contributions and allows tax-free withdrawals in retirement.

2. What are the 2025 contribution limits for 401(k) plans?

In 2025, you can contribute up to $23,000, or $30,500 if you’re age 50 or older and eligible for catch-up contributions.

Strategic Planning FAQs

3. Who benefits most from a Traditional 401(k)?

A Traditional 401(k) is generally best for those in higher tax brackets today who expect lower income (and lower taxes) in retirement.

4. Who should consider a Roth 401(k)?

A Roth 401(k) suits younger workers or anyone expecting higher taxes in the future. It offers tax-free income when you’ll likely need it most.

5. Can I split contributions between both types?

Yes. You can divide contributions between Traditional and Roth 401(k) accounts, as long as your total annual amount stays within IRS limits. This approach offers both short-term and long-term tax advantages.