You work for one of the most financially stable public authorities in New York State. While your colleagues in other government agencies worry about federal shutdowns and budget crises, you have something they don’t: financial independence.

The New York Power Authority generates its own revenue. You’re not funded by tax dollars. Your paycheck doesn’t depend on Albany’s budget battles or Washington’s political theater.

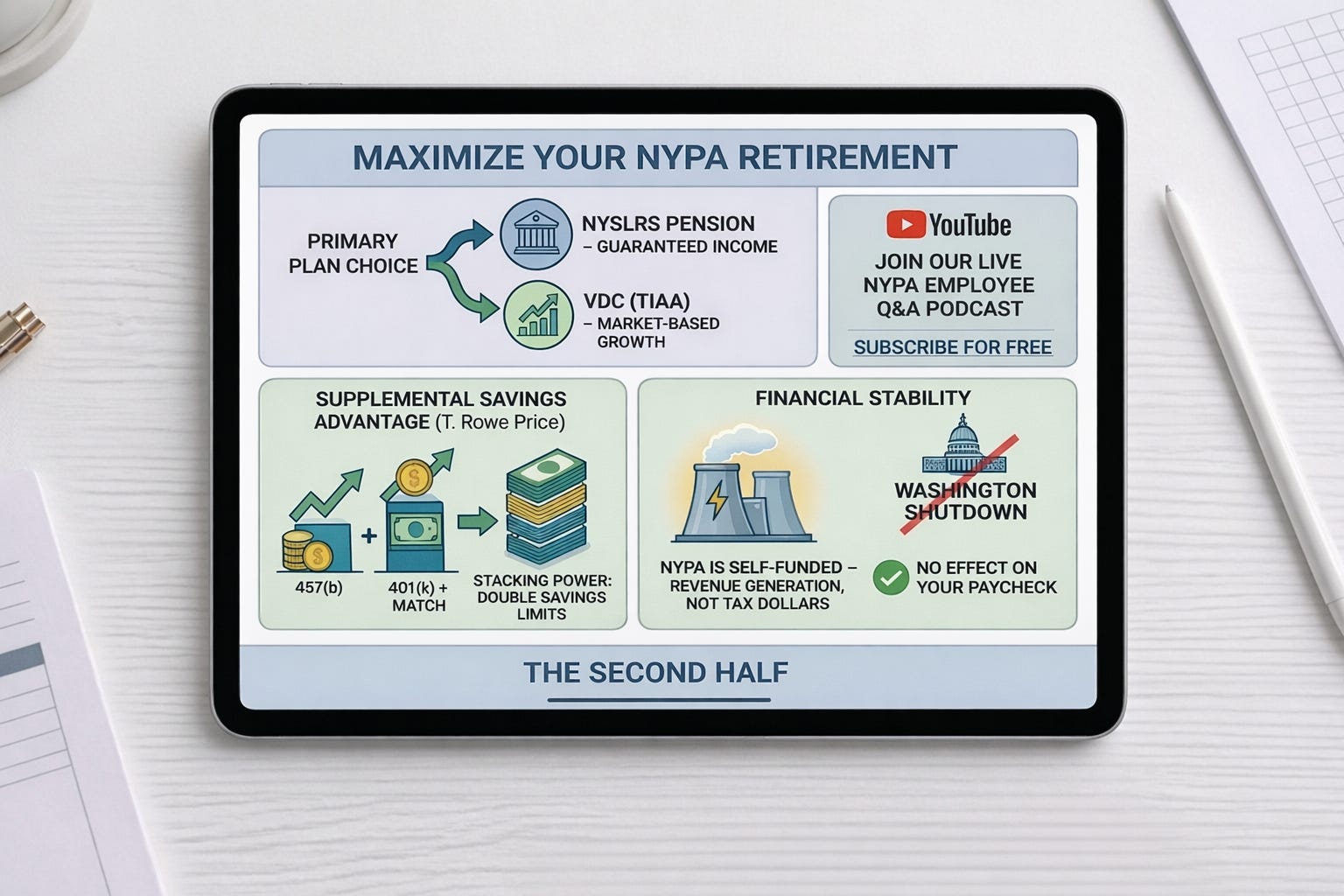

But here’s the paradox: despite having one of the most generous benefits packages in public service, most NYPA employees don’t fully understand what they have. The combination of NYSLRS pension options, the Voluntary Defined Contribution (VDC) Program, dual supplemental savings plans through T. Rowe Price and employer matching—it’s extraordinarily powerful, yet dangerously complex.

If you’re over 50 and reading this, you’re likely here for one of two reasons:

1. Desire: You’re ready for the next chapter and want to know if you can afford to retire early.

2. Fear: You hear news about “government shutdowns” and budget cuts and wonder if your job and pension are truly safe.

Let’s address the fear first: NYPA is self-funded from electricity revenue, not taxpayer money. A federal government shutdown does not affect your paycheck. However, there are real risks—state-level budget pressures, delays in federal funding for new infrastructure projects, and potential workforce restructuring—that require smart planning.

This guide will break through the confusion and explain every piece of your unique retirement system. From your primary pension choice to your “secret weapon” of dual savings plans (457b and 401k), you’ll understand exactly what you have and how to maximize it.

Critical first step: Before proceeding, you must know which employee group you belong to—Management, IBEW, or UWUA—as healthcare details and contribution rates differ significantly.

Section 1: Your Foundation – The Critical Primary

Retirement Plan Choice

For many NYPA employees, the most important financial decision of your career was made on your first day of work. You may not have fully understood it at the time, but that choice between two retirement paths shapes everything that follows.

Choice #1: The Guaranteed Pension (NYSLRS)

NYPA is a participating employer in the New York State and Local Retirement System (NYSLRS), managed by the NYS Comptroller. Most employees participate in the Employees’ Retirement System (ERS).

This is a defined benefit plan—a guaranteed lifetime income calculated by a formula: Final Average Salary × Years of Service × Tier Multiplier = Annual Pension

The critical advantage: the investment risk is borne by the State, not you. Market crashes don’t reduce your guaranteed pension. You know exactly what you’ll receive in retirement based on your salary and years of service.

Your tier determines everything:

● Tier 3 & 4 (hired 1976-2009): Generally age 55 with 30 years, or age 62 with 5 years for full pension

● Tier 5 (hired 2010-2011): Age 62 with 10 years

● Tier 6 (hired April 2012+): Age 63 with 10 years, with reduced benefits before that

Your pension calculation typically uses your highest 3 consecutive years of salary (Final Average Salary or FAS). Every year you work increases both your years of service and potentially your FAS, compounding your pension value.

Example: A Tier 4 employee with $90,000 FAS and 30 years of service receives approximately $45,000-54,000 annually for life, depending on tier multipliers.

Choice #2: The Market-Based Plan (VDC)

Employees earning over $75,000 had an irrevocable choice to opt out of NYSLRS and into the Voluntary Defined Contribution (VDC) Program.

This is a defined contribution plan (similar to a 401k), administered by TIAA. Your retirement benefit depends entirely on:

How much you and NYPA contribute

How you invest those contributions

Market performance over your career

You bear all the investment risk. Strong markets can produce larger retirement accounts than a pension. Poor markets or bad investment choices can leave you with far less.

The trade-off: VDC participants typically receive higher employer contributions (often 8-10% of salary) compared to the pension system. But there’s no guaranteed income—just whatever your account balance can generate.

Why This $75k+ Choice Was Your Most Important Career Decision

Two colleagues in the same role, hired the same day, could have vastly different financial futures 30 years later.

Colleague A (NYSLRS): Retires with a guaranteed $50,000/year pension that's inflation-protected and continues for life. No market risk. Peace of mind.

Colleague A (NYSLRS): Retires with a guaranteed $50,000/year pension that's inflation-protected and continues for life. No market risk. Peace of mind.

Colleague B (VDC): Retires with a $600,000 TIAA account. Must manage withdrawals carefully to avoid running out. Investment performance matters forever, not just during working years. More flexibility but more risk.

Neither choice is universally “better”—it depends on your risk tolerance, investment knowledge, and personal circumstances. But once made, this choice cannot be reversed.

If you chose VDC: Focus on maximizing contributions, proper asset allocation through TIAA, and withdrawal strategy planning. Consider working with a financial advisor who understands defined contribution plans.

If you chose NYSLRS: Focus on maximizing your FAS in your final years, understanding your tier’s rules, and building supplemental savings to complement your guaranteed pension.

Section 2: Your “Secret Weapon” – The Dual Supplemental Savings Plans (457b & 401k)

In addition to your primary retirement plan (NYSLRS or VDC), NYPA offers something incredibly rare and powerful: two separate supplemental savings plans that you can contribute to simultaneously.

This dual-plan structure gives NYPA employees a wealth-building advantage that most private-sector workers—and even most other government employees—simply don’t have.

Plan A: The New York Power Authority Deferred Compensation Plan (457 Plan)

This is a 457(b) plan administered by T. Rowe Price.

Key benefits of 457(b) plan

1. Tax advantages: Contributions are pre-tax (reducing your taxable income now) or Roth (tax-free withdrawals later).

2. 2025 contribution limits: $23,500 under age 50, $31,000 if age 50+ (with catch-up contributions).

3. The critical 457(b) advantage: Unlike 401(k)s or IRAs, 457(b) plans allow penalty-free withdrawals at any age after separation from service. No waiting until 59½. No 10% penalties.

This makes your 457(b) plan extraordinarily valuable for early retirement. If you retire at 55, you can access these funds immediately to bridge the gap until your NYSLRS pension or Social Security begins—without penalties.

Plan B: The Employees’ Savings Plan (401(k) Plan) with Employer Match

NYPA’s 401(k) plan includes the most valuable feature in retirement savings: employer matching.

The match structure: NYPA provides $0.50 for every dollar you contribute, up to the first 6% of your salary.

Example: If you earn $100,000 and contribute 6% ($6,000), NYPA adds $3,000. That’s a 50% guaranteed return before any investment growth. It’s free money.

2025 contribution limits: Same as 457(b)—$23,500 under age 50, $31,000 if age 50+.

Access rules: Unlike the 457(b), your 401(k) follows standard rules—withdrawals before 59½ typically face a 10% penalty unless you separate from service at age 55+.

The Strategic Advantage: How to “Stack” Contributions for Double Savings

Here’s where NYPA employees gain extraordinary advantage: Under IRS rules, 457(b) and 401(k) contribution limits are separate and independent.

This means you can contribute the maximum to both plans in the same year:

457(b): $31,000 (age 50+)

401(k): $31,000 (age 50+)

Total annual contributions: $62,000

A private-sector employee with just a 401(k) is limited to $31,000. You can save double that amount in tax-advantaged accounts—plus capture the 401(k) employer match.

Example of the compound advantage:

NYPA employee stacking both plans at age 50-65:

15 years × $62,000 = $930,000 in contributions

Plus employer 401(k) match: ~$45,000

Plus 15 years of compound growth at 7%: Total ≈ $1.8 million

Private-sector peer with only 401(k):

15 years × $31,000 = $465,000 in contributions

Plus similar match: ~$45,000

Plus growth: Total ≈ $900,000

The NYPA advantage: An extra ~$900,000 in retirement savings simply because you had access to dual plans.

Critical strategy for employees over 50: If you're not already maximizing both plans, this is your wake-up call. Every year you don't stack contributions is permanently lost compound growth.

Minimum requirement: At absolute minimum, contribute enough to your 401(k) to capture the full employer match (6% of salary). Failing to do so is leaving $3,000-6,000/year of free money on the table.

Got questions about your NYPA retirement?

Join our live NYPA Employee Q&A Podcast this November on YouTube. Ask about your pension, 457(b)/401(k) strategy, early retirement options, healthcare costs, or WEP/GPO impact—and get expert answers in real-time.

No sales pitch. Just NYPA-specific guidance, completely free.

Subscribe to our YouTube channel and follow us on social media for the date, time, and to submit your questions.

Section 3: Planning Your Exit – Voluntary vs. Involuntary Retirement

Now that you understand what you have, let’s address when and how you can retire. We must cover both scenarios: leaving on your own terms, or being forced out.

Scenario A: “I Want to Retire Early” (Voluntary Exit)

“Early” is defined by your NYSLRS tier rules. For Tier 6 employees, anything before 63 is early. For Tier 3/4 employees, you might achieve full pension at 55 with 30 years of service.

The critical question: Can you afford to stop working before your full pension and Social Security begin?

Building your income bridge:

Calculate your gap years: If you retire at 58 but don’t receive full pension until 62, that’s 4 years. If you delay Social Security to 67, that’s 9 years. How will you cover living expenses during this period?

Your bridge sources:

1. 457(b) withdrawals: Your primary bridge tool. Penalty-free at any age after separation. Calculate 3-4% annual withdrawals to preserve capital.

2. 401(k) withdrawals: Accessible penalty-free if you separate at 55+. Otherwise, wait until 59½.

3. Taxable savings: Maintain 12-18 months in accessible cash for emergencies and market downturns.

4. Part-time income: Many early retirees work part-time to reduce portfolio withdrawals and maintain social engagement.

Example bridge calculation:

Employee retiring at 58, full pension begins at 62:

Annual expenses: $60,000

Reduced NYSLRS pension if claimed early: $35,000

Annual gap: $25,000

4 years × $25,000 = $100,000 needed from 457(b)/401(k)

Plus buffer for healthcare and emergencies: $140,000 total

Healthcare is often the biggest obstacle: Before Medicare eligibility at 65, you’ll need private coverage. NYPA retiree healthcare (covered in Section 4) can cost $800-1,500/month depending on your employee group and plan selection.

Table: The early retirement decision matrix

✓ Green light if you have:

$500,000+ in combined 457(b)/401(k) accounts

Clear understanding of reduced pension for early claiming

Healthcare strategy to bridge to Medicare

Low debt and manageable fixed expenses

Specific plan for how you’ll spend your time

⚠ Proceed with caution if:

Less than $300,000 in supplemental savings High debt or financial obligations

Unclear healthcare costs

No plan beyond “I’m tired of working”

Scenario B: “What If I Have to Retire Early?” (Involuntary Exit)

Budget cuts. Workforce restructuring. Position elimination. While NYPA’s financial independence provides more stability than tax-funded agencies, no job is completely immune to organizational changes.

The buyout reality: NYPA does not have a permanent, standing buyout program. What you might hear called “buyouts” are actually temporary, state-legislated programs called Early Retirement Incentives (ERI).

These are “windows of opportunity” that the state legislature opens (like in 2010) and NYPA can choose to opt into. An ERI typically offers:

Additional years of service credit (often 3 years)

Time-limited acceptance window (30-60 days)

Age and service minimums to qualify

The critical point: ERIs are rare and unpredictable. You might never see one during your career, or one might be offered next year. The only certainty is that you must be financially prepared before a window opens.

If an ERI is offered, you’ll face rapid decision-making:

Calculate whether 3 additional service years make early retirement viable

Assess pension amount with incentive vs. continuing to work

Analyze healthcare bridge costs if you’re under 65

Evaluate the probability of remaining in your position if you decline

Make an irrevocable decision in 30-60 days

The involuntary exit preparation strategy:

Know your numbers: Get a current NYSLRS pension estimate. Understand exactly what you’d receive if separated today vs. in 2, 5, or 10 years.

Maximize contributions: If there’s any possibility of involuntary separation, max out both 457(b) and 401(k) now. Every dollar saved today is a dollar you won’t need to earn tomorrow.

Build liquidity: Maintain 18-24 months of expenses in accessible cash. This buffer allows you to avoid selling investments during market downturns and gives you negotiating power.

Understand your options: Know your tier’s rules, early claiming penalties, and healthcare continuation requirements before you’re forced to make rushed decisions.

Consider transfers: NYPA has multiple locations and departments. If your position becomes vulnerable, proactive transfer requests to more secure areas might be possible.

Got questions about your NYPA retirement?

Join our live NYPA Employee Q&A Podcast this November on YouTube. Ask about your pension, 457(b)/401(k) strategy, early retirement options, healthcare costs, or WEP/GPO impact—and get expert answers in real-time.

No sales pitch. Just NYPA-specific guidance, completely free.

Subscribe to our YouTube channel and follow us on social media for the date, time, and to submit your questions.

The peace-of-mind threshold: Most NYPA employees with $500,000+ in combined 457(b)/401(k) accounts and 20+ years toward their pension can weather involuntary separation without financial catastrophe—assuming they've planned properly.

Section 4: The Two Biggest Retirement Decisions: Healthcare & Social Security

A successful retirement isn’t just about having enough money—it’s about managing your two biggest ongoing costs and risks: healthcare and Social Security integration.

Your Retiree Healthcare: A Critical Distinction

NYPA provides retiree healthcare through specific plan options that you’ll recognize: UnitedHealthcare (UHC), CDPHP, Independent Health, and prescription coverage through SilverScript.

Critical clarification: NYPA does not participate in the statewide NYSHIP (New York State Health Insurance Program). This is a common point of confusion. Your healthcare is separate from what state employees receive.

Costs vary significantly by employee group:

Management employees typically pay higher premiums

IBEW and UWUA members have negotiated rates through collective bargaining

Your HR department has specific rate schedules for your group

Eligibility for retiree coverage:

Generally requires retirement directly from NYPA (not just separation)

Must meet NYSLRS retirement eligibility (immediate retirement, not deferred)

Coverage can continue for life if maintained continuously

The Medicare transition at 65: Your NYPA retiree coverage coordinates with Medicare. At 65, you’ll typically enroll in Medicare Parts A and B, and your NYPA coverage becomes supplemental. This coordination usually reduces your premiums.

Healthcare cost planning:

Ages 55-65 (before Medicare): Budget $800-1,500/month depending on your employee group and coverage level. For a couple both under 65, this could be $15,000-30,000/year—often the largest expense in early retirement.

Ages 65+ (with Medicare): Costs typically drop to $300-600/month for Medicare premiums plus supplemental coverage, or $7,000-15,000/year for a couple.

⚠️ CRITICAL EXCEPTION: NYS Canal Corporation Employees

Are you an employee of the NYS Canal Corporation?

If so, this healthcare section does not apply to you. As a NYPA subsidiary, the Canal Corporation participates in the NYSHIP program (New York State Health Insurance Program).

Your retiree healthcare rules, coverage options, and costs are completely different from NYPA employees. Please contact your HR department for NYSHIP-specific details, or visit the NYS Department of Civil Service website.

Do not make retirement healthcare decisions based on NYPA plan information—it does not apply to Canal Corporation employees.

Social Security and Your NYPA Pension: Understanding WEP & GPO

Here’s where many NYPA retirees get blindsided: receiving an NYSLRS pension can have a major, unexpected impact on your Social Security benefits.

Two rules can reduce or eliminate your Social Security

Windfall Elimination Provision (WEP):

Reduces your own personal Social Security benefit if you receive a pension from work where you didn’t pay Social Security taxes

Can reduce Social Security by up to $587/month (2025 maximum)

Affects employees who paid into Social Security from other jobs (before or after NYPA)

Example: You worked in the private sector for 15 years (paying Social Security taxes), then joined NYPA for 25 years (NYSLRS pension, no Social Security taxes). When you claim Social Security based on your 15 private-sector years, WEP can reduce your benefit by $300-500/month for life.

Government Pension Offset (GPO):

Reduces or eliminates spousal or survivor Social Security benefits

Reduces spousal/survivor benefits by two-thirds of your government pension amount

Can completely eliminate spousal benefits if your pension is high enough

Example: Your spouse worked in the private sector and receives $2,000/month Social Security. Normally, you could claim a $1,000/month spousal benefit. But if your NYSLRS pension is $1,800/month, GPO reduces your spousal benefit by $1,200 (2/3 × $1,800). Since $1,200 is more than the $1,000 spousal benefit, you receive zero from Social Security as a spouse.

WEP/GPO impact over retirement:

If WEP reduces your Social Security by $400/month starting at age 62:

30-year retirement: $400 × 12 months × 30 years = $144,000 lifetime reduction

If GPO eliminates a $1,000/month spousal benefit:

25-year retirement: $1,000 × 12 months × 25 years = $300,000 lifetime loss

Who is affected:

VDC participants typically don’t face WEP/GPO because NYPA withholds Social Security taxes from their pay

NYSLRS participants do face WEP/GPO risk because NYSLRS is a non-Social Security covered pension

Check your pay stub: if Social Security taxes (FICA) are withheld, you’re likely exempt from WEP/GPO

Strategic responses:

If WEP applies to you: Consider delaying Social Security to age 70 to maximize the base benefit before WEP reduction is applied. Every year you delay increases the benefit by 8%, somewhat offsetting WEP’s impact.

If GPO applies: Understand that claiming your own Social Security benefit (if you have one) versus claiming as a spouse produces different results under GPO. Run the calculations for both scenarios.

Critical planning requirement: WEP and GPO calculations are complex and often misunderstood. Do not estimate these on your own. Consult with a financial advisor who specializes in public pensions and understands these provisions before making claiming decisions.

A $200,000-300,000 mistake in Social Security timing is entirely preventable with proper analysis—but only if you know WEP/GPO applies to you before you claim.

From NYPA Complexity to Retirement Confidence

You have one of the most powerful benefits packages in the country:

NYSLRS guaranteed pension or VDC flexibility through TIAA

Dual supplemental savings (457b through T. Rowe Price + 401k with match)

Ability to save $62,000/year in tax-advantaged accounts

Retiree healthcare continuation

Financial stability of a self-funded authority

But with this power comes complexity. Making the wrong decisions can cost you hundreds of thousands of dollars:

Choosing VDC without understanding the risk

Failing to “stack” contributions to both 457(b) and 401(k)

Retiring early without a proper income bridge strategy

Being blindsided by WEP/GPO Social Security reductions

Misunderstanding retiree healthcare eligibility and costs

Missing a rare ERI window because you weren’t prepared

This guide is your foundation. The next step is building a plan specific to you. Your personal financial independence date depends on variables this article cannot address:

Your specific tier and years of service

Your current 457(b) and 401(k) balances

Your employee group’s healthcare costs

Your Social Security work history and WEP/GPO status

Your spouse’s income and benefits

Your debt, expenses, and retirement lifestyle goals

These calculations require precision, not guesswork.

Whether you’re planning a voluntary early retirement or preparing for an unexpected ERI offer, the cost of specialized guidance ($2,000-5,000 for comprehensive NYPA-specific analysis) is minimal compared to the six-figure decisions at stake.

Ready to calculate your true financial independence date?

Schedule a complimentary analysis of your personal NYPA situation. We’ll review your pension estimate, evaluate your 457(b) and 401(k) positioning, model your healthcare bridge to Medicare, calculate WEP/GPO impact, and determine exactly when you can retire with confidence.

Click here to schedule your consultation, or join our live call-in podcasts this November and December on YouTube for free expert guidance on NYPA retirement planning, dual-plan optimization, and other critical public pension topics.