The Hidden Truth About Why Your 401k Won't Be Enough for Retirement, And What to Do Instead

You’ve been contributing to your 401k for years. You’ve watched the balance grow. You feel good about your retirement savings. But here’s the uncomfortable truth most financial advisors won’t tell you: your 401k alone probably won’t be enough.

The numbers are more alarming than you think. According to recent studies, the median 401k balance for Americans aged 55-64 is under $250,000. That might sound substantial, but using the 4% withdrawal rule, that’s only $10,000 per year in retirement income. Can you live on $833 per month? And that 4% rule doesn’t hold up, especially in times of higher inflation and cost of living. Right now that # is closer to 6%. The higher the withdrawal rate the faster you run out of money.

The 401k System Wasn’t Designed for Full Retirement Funding

Here’s what most people don’t realize.

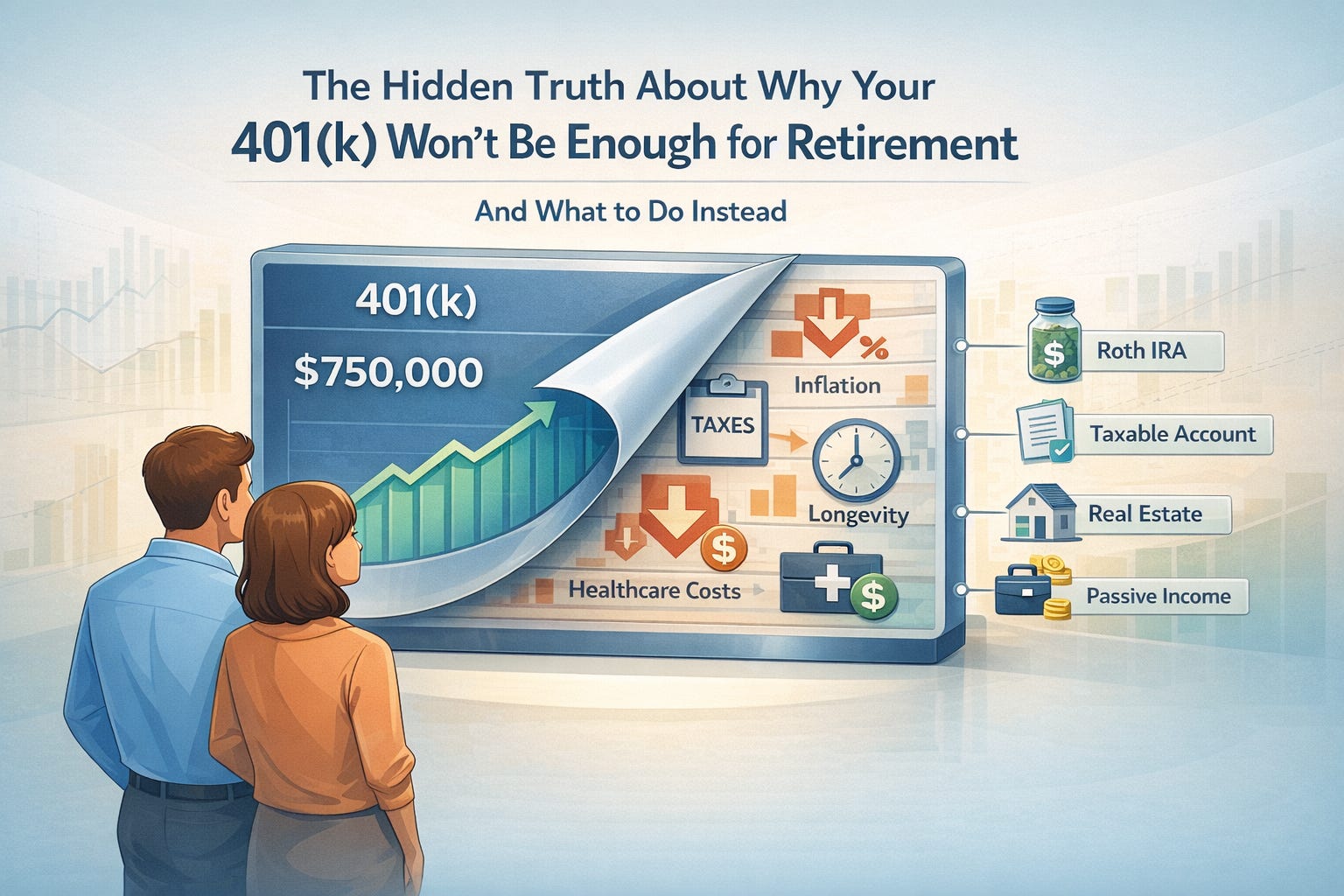

401ks were originally designed as a supplement to pensions and Social Security, not as the primary retirement vehicle. When the first 401k plan was created in 1978, it was meant to be the third leg of a three-legged retirement stool. But pensions have largely disappeared, Social Security benefits are under pressure, and suddenly your 401k is carrying weight it was never meant to bear.

The harsh reality:

● 401k contribution limits cap your savings potential

● Market volatility can devastate your balance right before retirement

● Required minimum distributions force you to withdraw money whether you need it or not

● No guaranteed income stream for life

● Healthcare costs can quickly drain your savings

Why Traditional Retirement Advice Falls Short

Walk into any major financial firm with less than $5 million, and you’ll get the same cookie-cutter advice: “Max out your 401k, invest in index funds, and hope for the best.” This one-size-fits-all approach ignores your unique situation, risk tolerance, and actual income needs in retirement.

The problems with generic advice:

● Doesn’t account for sequence of returns risk

● Ignores tax diversification strategies

● Fails to address longevity risk

● No consideration for changing expenses in retirement

● Lacks flexibility for unexpected costs

Beyond the 401k: Building True Retirement Security

A complete retirement income strategy goes beyond just accumulation. It requires:

1. Income diversification across multiple sources

2. Tax diversification across different account types

3. Time diversification through each stage of retirement

4. Risk management for healthcare and long-term care costs

5. Legacy planning for your heirs

Warning Signs Your Retirement Plan Needs Help

You might need more than just a 401k if:

● You’re within 10 years of retirement with less than 10 times your annual expenses saved

● You’re within 3 years of retirement with less than 15 times your annual expenses saved

● You haven’t optimized your Social Security claiming strategy

● You have no plan for healthcare costs in retirement

● You don’t have a detailed income and expense plan pre and post retirement

● You’re getting generic advice from your current advisor

The Cost of Waiting

Every month you delay addressing these issues is a month of potential income lost in retirement. The closer you get to retirement, the less time you have to course-correct.

Consider this: A 50-year-old who implements a comprehensive retirement income strategy has 15 years to optimize their approach. A 60-year-old has just 5 years. The difference in outcomes can be hundreds of thousands of dollars in lifetime income.

Take Action: Your Next Steps

Your 401k is a good start, but it’s not the finish line. True retirement security requires a comprehensive approach that addresses income, taxes, healthcare, and legacy planning.

At RetireNova, we specialize in creating predictable, sustainable retirement income for people who’ve been told they don’t have “enough” for personalized attention. We believe everyone deserves a retirement plan that’s built for their unique situation – not a generic strategy that treats you like a number.

The NOVA 3-Bucket Alternative: A Better Way Forward

At RetireNova, we’ve developed a different approach. Instead of putting all your eggs in the 401k basket, we create predictable, sustainable income through our proven 3-Bucket System:

Bucket 1: Safety & Stability (Years 1-7) Your retirement paycheck for the next 7 years. This bucket holds conservative investments and fixed-income products that provide consistent, dependable income with minimal volatility. You shouldn’t have to worry about this bucket – just like you don’t worry about your current paycheck.

Bucket 2: Moderate Growth (Years 8-15) This bucket refills Bucket 1 when it runs low. It contains a balanced mix of conservative and growth assets designed to manage moderate risk while keeping funds growing over the medium term. This money won’t be touched for at least 7 years, giving it time to grow.

Bucket 3: Long-Term Growth (Years 16+) Your long-term growth engine. This bucket holds growth-oriented investments designed to outpace inflation and grow your assets over time. We’re investing this for a much later stage of retirement, giving it maximum time to compound.

Ready to see what your retirement could really look like?

Book a complimentary 30-minute consultation with one of our retirement income specialists. We’ll review your current situation, identify gaps in your strategy, and show you exactly how our 3-Bucket System can provide the predictable income you need to retire with confidence.

No sales pitch. Just honest guidance from advisors who put your interests first.