The decision of when to claim Social Security could be worth more than your 401(k).

Most people treat Social Security as an afterthought – something that just “kicks in” when they retire. But this casual approach to your largest guaranteed income source in retirement can cost you hundreds of thousands of dollars in lifetime benefits.

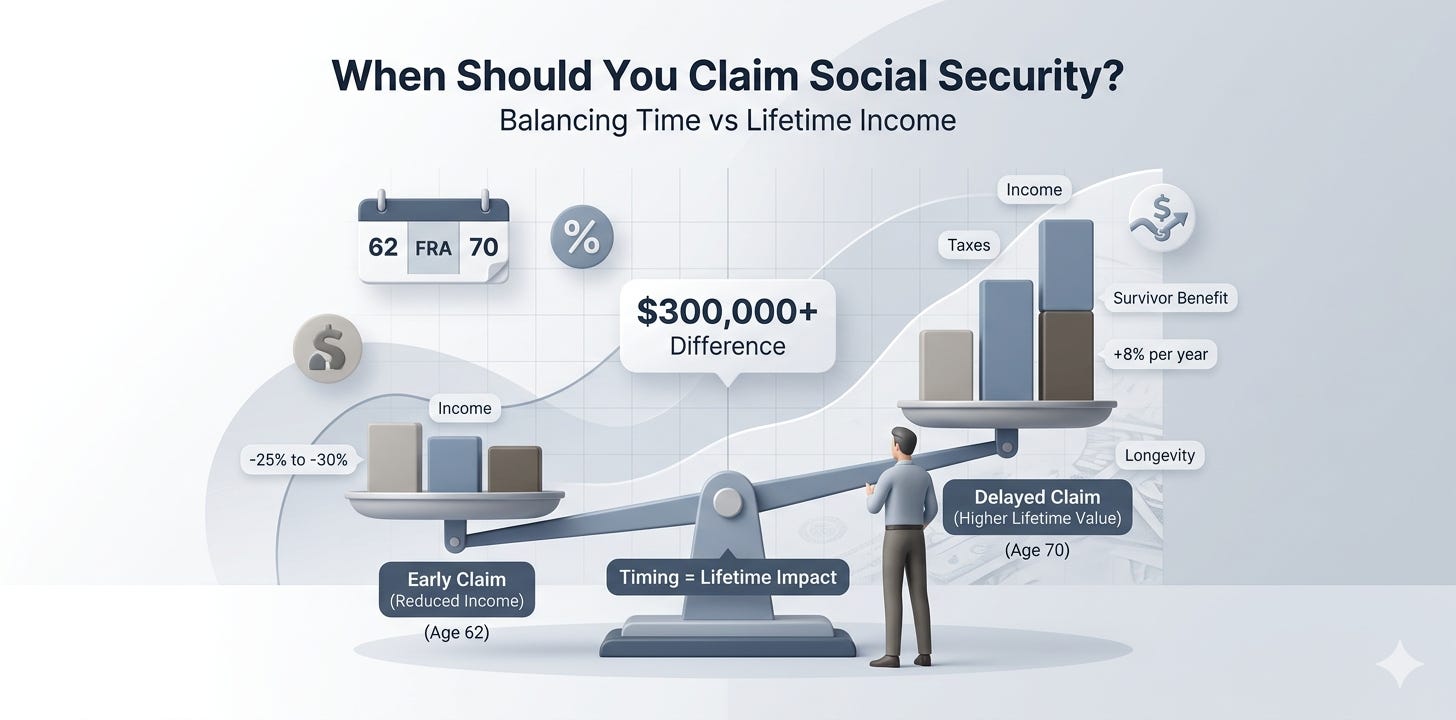

The difference between optimal and suboptimal Social Security timing often exceeds $300,000 for married couples. Yet 96% of Americans claim benefits at the wrong time, leaving massive amounts of money on the table.

The $300,000 Question: When Should You Claim?

Here’s the brutal math most people miss:

John, age 62, eligible for $2,000/month at full retirement age (67):

If he claims at 62: $1,400/month ($16,800/year)

If he claims at 67: $2,000/month ($24,000/year)

If he claims at 70: $2,640/month ($31,680/year)

Lifetime difference between claiming at 62 vs. 70:

● Age 62 strategy: $353,400 total through age 85

● Age 70 strategy: $507,840 total through age 85

● Lost income: $154,440 for a single person

For married couples, the math gets even more dramatic because of spousal and survivor benefits.

The Emotional vs. Mathematical Decision

Why do so many people claim early despite the huge financial cost?

Common (expensive) reasoning:

● “I want to get my money before Social Security goes broke”

● “A bird in the hand is worth two in the bush”

● “I don’t trust the government to keep paying”

● “What if I die early?”

● “I need the money now to retire”

The reality:

● Social Security has never missed a payment in 80+ years

● Even worst-case scenarios show 75-80% benefits continuing

● The break-even analysis favors delayed claiming for most people

● Early claiming often forces suboptimal retirement portfolio withdrawals

The Full Retirement Age Confusion

Most people don’t understand how their “full retirement age” (FRA) affects their benefits:

If you were born:

● 1943-1954: FRA is 66

● 1955: FRA is 66 and 2 months

● 1956: FRA is 66 and 4 months

● 1957: FRA is 66 and 6 months

● 1958: FRA is 66 and 8 months

● 1959: FRA is 66 and 10 months

● 1960 or later: FRA is 67

Claiming before FRA: Benefits reduced by 5/9 of 1% for each month up to 36 months early, then 5/12 of 1% for each additional month

Claiming after FRA: Benefits increase by 8% per year until age 70 (called Delayed Retirement Credits)

Critical insight: There’s no benefit to delaying past age 70 – that’s when you should definitely start claiming.

The Married Couple Optimization Goldmine

Single people have it relatively simple compared to married couples, who have multiple claiming strategies that can dramatically impact lifetime benefits.

Available strategies for married couples:

● Claim and invest: One spouse claims early, invests the benefits

● Split timing: One spouse claims at FRA, other delays to 70

● Maximize the survivor benefit: Higher earner delays to 70 to maximize widow(er) benefits

● File and suspend: (No longer available for new claims, but important to understand for those grandfathered)

Case Study: The $287,000 Optimization

Background: Mark and Lisa, both age 62

● Mark’s benefit at FRA (67): $2,800/month

● Lisa’s benefit at FRA (67): $1,200/month

● Both in good health with longevity in their families

Suboptimal strategy (what most people do):

● Both claim at 62

● Mark gets $1,960/month, Lisa gets $840/month

● Combined: $2,800/month ($33,600/year)

Optimized strategy:

● Lisa claims at FRA (67): $1,200/month

● Mark delays until 70: $3,472/month

● Combined at age 70: $4,672/month ($56,064/year)

The difference:

● Additional income: $22,464 per year

● Over 20 years: $449,280 more in total benefits

● Even accounting for the delayed start, lifetime benefit difference: $287,000

Plus: When Mark dies, Lisa receives his full $3,472/month as a survivor benefit instead of $1,960/month – an additional $1,512/month for the rest of her life.

The Widow(er) Benefit Strategy Most People Miss

This is perhaps the most important Social Security optimization for married couples: When one spouse dies, the surviving spouse receives the higher of:

● Their own benefit, or

● 100% of their deceased spouse’s benefit

Strategic implication: The higher-earning spouse should almost always delay claiming until 70 to maximize the survivor benefit.

Real example: If the higher earner dies at 75:

● Claimed at 62: Survivor gets $1,960/month for life

● Claimed at 70: Survivor gets $3,472/month for life

● Difference: $1,512/month for potentially 15+ years = $272,160

The Health Factor: When Early Claiming Makes Sense

You should consider claiming early if:

● You have serious health conditions with life expectancy below 78-80

● You need the income immediately and have no other options

● You’re unemployed and need bridge income until finding work

● You have a much younger spouse (complex optimization needed)

The break-even analysis:

● Claiming at 62 vs. FRA: Break-even around age 78

● Claiming at FRA vs. 70: Break-even around age 82

Key insight: Average life expectancy at 65 is 84 for men, 87 for women. Most people will live long enough to benefit from delayed claiming.

The Working in Retirement Penalty

If you claim Social Security before FRA and continue working:

2024 earnings test:

● If you’re under FRA: $1 in benefits withheld for every $2 earned above $22,320

● In the year you reach FRA: $1 withheld for every $3 earned above $59,520 (only months before FRA count) ● After FRA: No earnings penalty

Important: Withheld benefits aren’t lost forever – they’re recalculated into higher future benefits. But this creates cash flow challenges for many retirees.

The Tax Optimization Angle

Social Security benefits become taxable when your “combined income” exceeds certain thresholds:

Single filers:

● $25,000-$34,000: Up to 50% of benefits taxable

● Above $34,000: Up to 85% of benefits taxable

Married filing jointly:

● $32,000-$44,000: Up to 50% of benefits taxable

● Above $44,000: Up to 85% of benefits taxable

Strategic opportunity: Coordinating Social Security timing with retirement account withdrawals can minimize lifetime taxes.

Advanced Strategies: Beyond Basic Timing

Roth Conversion Coordination: Delay Social Security while doing Roth conversions in low-tax years, then claim higher benefits later while enjoying tax-free Roth income.

Tax-Location Strategy: Use taxable account withdrawals during Social Security delay period to minimize overall tax burden.

Healthcare Considerations: Coordinate claiming with Medicare enrollment and potential premium penalties.

State Tax Planning: Some states don’t tax Social Security benefits, creating relocation opportunities.

The “Social Security Is Going Broke” Myth

The facts:

● Social Security’s trust fund is projected to be depleted around 2034

● Even then, ongoing payroll taxes would fund approximately 80% of benefits

● Congress has always acted to preserve benefits (happened in 1977, 1983)

● Possible solutions include raising the cap on taxable wages, modest benefit adjustments, or small tax increases

Bottom line: Social Security isn’t going away, and optimization strategies remain crucial regardless of future adjustments.

Red Flags: Signs You Need Social Security Optimization Help

You should get professional help if:

● You’re married and haven’t analyzed spousal strategies

● You’re planning to claim as soon as you retire

● You haven’t considered the impact on survivor benefits

● You’re working in retirement and claiming benefits

● You haven’t coordinated Social Security with your overall tax strategy

● You’re divorced and unsure about ex-spouse benefits

The DIY Trap: Why Online Calculators Aren’t Enough

Basic Social Security calculators miss crucial factors:

● Spousal optimization strategies

● Tax implications of different timing choices

● Coordination with retirement account withdrawals

● Impact on Medicare premiums (IRMAA surcharges)

● State tax considerations

● Longevity and health factors

Professional optimization software considers hundreds of variables and scenarios that online calculators simply can’t handle.

Your Next Steps: Getting Your Social Security Strategy Right

Social Security optimization is complex, but the financial impact is too large to ignore. The difference between good and bad timing can easily fund several additional years of retirement.

At RetireNova, our Social Security optimization analysis includes:

● Comprehensive benefit projections for all claiming strategies

● Spousal and survivor benefit optimization

● Tax-efficient coordination with retirement withdrawals

● Medicare premium impact analysis (IRMAA considerations)

● Longevity and health factor modeling

● Clear recommendations with supporting rationale

We use advanced software that analyzes thousands of scenarios to find your optimal strategy. Ready to discover how much your Social Security optimization could be worth?

[Schedule Your Complimentary Social Security Analysis]

Our analysis typically identifies $50,000-$300,000 in additional lifetime benefits for married couples – money that’s rightfully yours but often left on the table due to poor timing decisions.

Because when it comes to Social Security, timing isn’t everything – it’s the only thing.