Social Security COLA stands for Cost‑of‑Living Adjustment — an annual increase in Social Security and Supplemental Security Income (SSI) benefit amounts intended to help benefits keep pace with inflation. COLAs are mandatory when inflation rises, and they protect benefit purchasing power over time by adjusting payouts based on changes in the Consumer Price Index. Social Security

Why COLA Matters

● COLA is designed to offset inflation so beneficiaries do not lose ground as prices rise. Social Security

● The adjustment applies automatically if the CPI‑W (Consumer Price Index for Urban Wage Earners and Clerical Workers) increases from one period to the next. Social Security

● COLA applies not only to retirement benefits but also to disability and SSI payments. Social Security

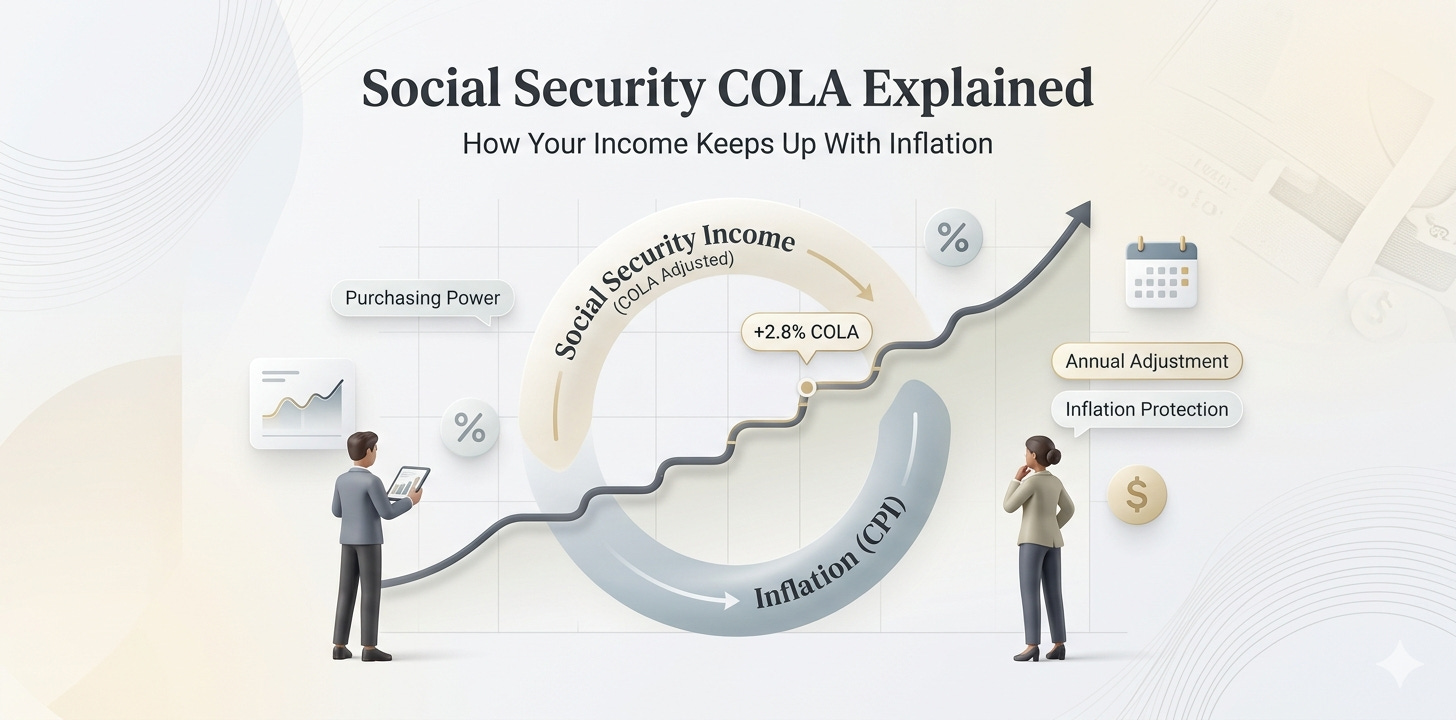

Recent and Current COLA

● For 2026, the SSA announced a 2.8 % COLA effective with benefits paid beginning January 2026 — meaning retirees and other beneficiaries will see a roughly 2.8 % increase in their monthly benefit. Social Security

● This 2.8 % rise is slightly above recent COLAs (e.g., 2.5 % in 2025) but below long‑term historical averages.

What COLA Does and Does Not Do

● A COLA increases your benefit amount, but it does not always fully match retirees’ actual cost increases, especially for healthcare and out‑of‑pocket expenses not well captured by CPI‑W. Encyclopedia Britannica

● COLA is not guaranteed every year — if measured inflation does not rise, there may be no COLA. Social Security

TACTICAL PLAN: How to Incorporate COLA Into Retirement Planning

Step 1 — Know the COLA for the Current and Coming Year

● Check the latest SSA announcement or trusted sources around October/November each year — this is when the COLA is usually announced. Social Security

● For 2026, expect a 2.8 % increase in benefits beginning with your January payment. Social Security

Step 2 — Project Benefit Income After COLA

● Multiply your current benefit by 1.028 to estimate your new monthly amount. (Example: $2,000 × 1.028 = $2,056.)

● Remember COLA applies on the entire benefit amount you currently receive, not just a portion.

Step 3 — Coordinate with Medicare Premiums

● Medicare Part B premiums are deducted from Social Security checks. Rising premiums can offset some or all of your COLA increase. Budget for this before assuming extra cash flow.

Step 4 — Update Your Retirement Income Plan

● Enter the new benefit amount and associated tax impacts into your retirement cash‑flow model so you understand how the COLA influences long‑term projections.

Step 5 — Adjust Withholding and Tax Planning

● Increased benefits may affect your taxable income and the portion of Social Security that’s taxable. Adjust withholding or estimated taxes if needed.

Step 6 — Consider Inflation Assumptions

● Because COLA is based on CPI‑W (which can lag retirees’ actual cost increases), supplement Social Security income with other inflation‑adjusted sources (e.g., part of a diversified investment portfolio).

Step 7 — Monitor Future COLA Paths

● COLA amounts vary yearly based on actual inflation data. Review your plan annually and adjust spending and saving strategies accordingly.

TOP 10 FAQs (With Answers)

1. What is the Social Security COLA?

It’s a Cost‑of‑Living Adjustment that increases Social Security benefits if inflation (measured by the CPI‑W) has risen over a specified period. Social Security

2. When does the COLA take effect?

COLA increases are effective in December of the current year and reflected in January benefit payments of the following year. Social Security

3. How much is the 2026 COLA?

The 2026 COLA is 2.8 %, meaning monthly benefits are increased by that percentage starting in January 2026. Social Security

4. Does everyone get the same COLA percentage?

Yes — all Social Security and SSI beneficiaries get the same percentage increase, though the dollar amount depends on each person’s benefit level. Social Security

5. Can a COLA be zero?

Yes — if inflation as measured by CPI‑W doesn’t rise over the measurement period, there may be no COLA that year. Social Security

6. Does COLA always keep pace with my actual costs, like healthcare?

Not always. CPI‑W may understate some retirees’ out‑of‑pocket costs (especially medical expenses), so COLA may not fully maintain purchasing power. Encyclopedia Britannica

7. Can Medicare premiums offset my COLA increase?

Yes. Medicare Part B premiums are deducted from your benefit, and if they rise sharply, they can eat into or exceed the COLA bump. (This has happened in recent years.) Kiplinger

8. How do I estimate my new benefit after COLA?

Multiply your current monthly benefit by 1 + COLA% (e.g., × 1.028 for a 2.8 % COLA). Social Security

9. Does COLA apply to all Social Security benefits?

Yes — COLA applies to retirement, disability, and Supplemental Security Income (SSI) benefits. Social Security

10. Where can I find the most current COLA announcement?

The Social Security Administration’s official website publishes COLA notices and latest COLA figures, typically in mid‑to‑late October. Social Security