When you save for retirement through accounts like a 401(k) or IRA, the IRS eventually requires you to begin taking money out. These withdrawals are known as Required Minimum Distributions, or RMDs. The purpose of RMD rules is simple: retirement accounts give you tax advantages while you’re working, but the government wants to collect taxes once you reach a certain age.

RMD rules apply to most retirement accounts, including traditional IRAs, 401(k)s, 403(b)s, and other tax-deferred plans. Inherited accounts, including inherited Roth IRAs, also follow special distribution rules. If you don’t take your RMD on time, the penalties can be costly.

What Are Required Minimum Distributions?

Required Minimum Distributions are the minimum amounts you must withdraw each year from certain retirement accounts once you reach the required age. The IRS enforces these withdrawals to make sure tax-deferred savings eventually become taxable income.

Under IRS required minimum distribution (RMD) rules, both traditional IRAs and employer plans such as 401(k)s and 403(b)s are covered. Roth IRAs are different; while they don’t require RMDs during the original owner’s lifetime, inherited Roth IRAs do come with mandatory withdrawals. This distinction is important for families planning to pass down wealth.

In short, if you hold a tax-deferred retirement account, you cannot keep your money growing tax-free forever. Once you reach the RMD age, you’ll need to start withdrawals based on an IRS formula tied to life expectancy.

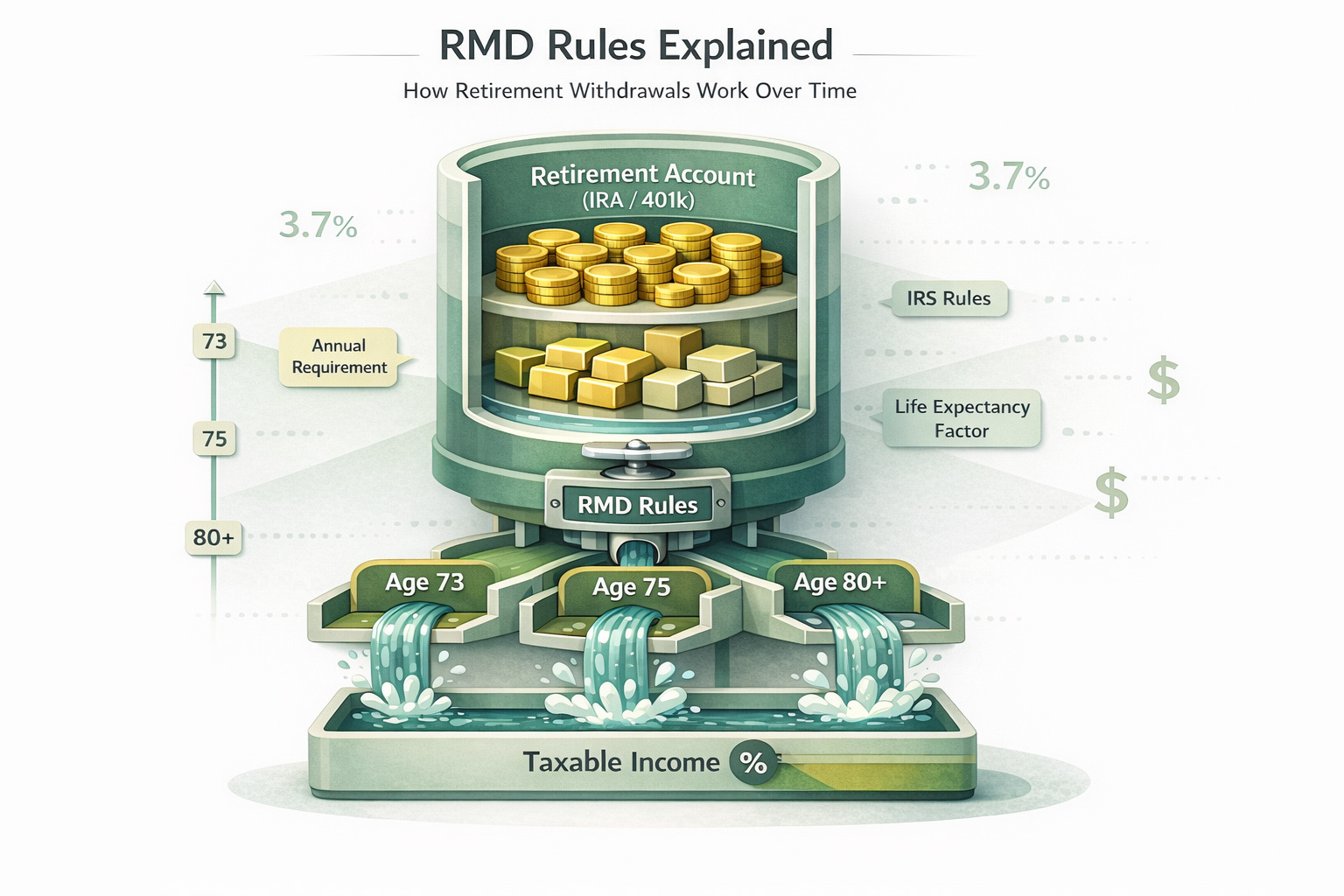

RMD Rules by Age: Understanding When Withdrawals Start

The age when you must start taking Required Minimum Distributions has changed in recent years. For many years, the rule was that withdrawals had to begin at age 72. However, the SECURE Act 2.0 raised the starting age to 73 for anyone who reaches 72 after 2022. This adjustment gives retirees a little more time to keep their savings invested before being required to withdraw.

The IRS also sets strict deadlines. Your first RMD must be taken by April 1 of the year following the year you reach your required starting age. For example, if you turn 73 in 2025, you can delay your first withdrawal until April 1, 2026. However, waiting means you may have to take two distributions in that same year, one by April and one by December 31, which could push you into a higher tax bracket.

After your first year, all RMD requirements by age follow the same schedule: you must withdraw by December 31 each year. Missing the deadline can trigger a steep IRS penalty. That’s why it is important to know exactly when your withdrawals begin and how to manage the timing.

RMD Schedule for IRA and 401(k) Accounts

Once you reach the RMD age, withdrawals become an annual requirement. The IRS schedule is straightforward: every year you must take out at least the minimum amount calculated from your account balance and life expectancy factor.

This rule applies to both IRAs and 401(k) accounts, although the details can differ. If you have multiple IRAs, you can calculate the total RMD and take it from just one account if you prefer. With 401(k)s, however, you must take a required distribution from each plan separately, unless you have rolled them into one.

The 401k RMD rules for 2025 are the same as for other years; the only change that may apply to you is the age threshold, depending on your birth year. Every RMD must be completed by December 31, with the exception of the first year’s April 1 extension.

RMD Tables Explained

To calculate your RMD, the IRS provides specific life expectancy tables. These tables determine the percentage of your account that must be withdrawn each year.

Most retirees use the Uniform Lifetime Table, which applies if you are the sole owner of the account or if your spouse is not more than ten years younger than you. This table lists divisors that correspond to your age, which are then used to calculate the withdrawal amount.

If your spouse is more than ten years younger and is your sole beneficiary, the IRS allows you to use the Joint Life and Last Survivor Table, which often results in smaller required withdrawals. This can help preserve retirement savings for couples with a significant age gap.

For beneficiaries of inherited IRAs, the Single Life Expectancy Table applies. This table is also based on age, but it follows different rules for inherited accounts.

RMD Quick Guide by Age

Age 72 → 3.65% (Factor: 27.4)

Age 73 → 3.77% (Factor: 26.5)

Age 75 → 4.07% (Factor: 24.6)

Age 80 → 4.95% (Factor: 20.2)

Age 85 → 6.25% (Factor: 16.0)

Age 90 → 8.20% (Factor: 12.2)

How to Calculate Your RMD (Step-by-Step Guide)

The process of calculating your Required Minimum Distribution follows a simple formula:

Account balance at year-end ÷ Life expectancy factor = RMD amount

Your account balance is based on the value of your IRA or 401(k) as of December 31 of the previous year. The life expectancy factor comes from the IRS table that applies to your situation.

For example, suppose you are 73 years old with an IRA balance of $200,000 on December 31. According to the IRS Uniform Lifetime Table, the life expectancy factor for age 73 is 26.5. Divide $200,000 by 26.5, and your required minimum distribution for the year would be $7,547.

Accuracy is very important in this process. Using the wrong balance or factor could mean under-withdrawing, which might expose you to IRS penalties. That is why retirees often rely on calculators, custodians, or financial planners to verify the figures.

IRS Penalties and Tax Rules for RMDs

The IRS takes RMD compliance seriously. If you miss a required withdrawal, the penalty is steep: 25 percent of the amount you should have taken out. For example, if your RMD was $10,000 and you failed to withdraw, the penalty could be $2,500. If corrected promptly, the IRS may reduce this penalty to 10 percent, but it is better to avoid the issue altogether.

All RMDs are taxed as ordinary income, not as capital gains, regardless of whether the money comes from an IRA or a 401(k). This means the withdrawal amount is added to your taxable income for the year and taxed at your current rate.

In terms of reporting, your plan provider will issue Form 1099-R, which lists the distribution. You must include this when filing your tax return. Following IRS 401k RMD rules carefully helps retirees stay compliant, avoid penalties, and manage tax liability in retirement.

RMD Planning Strategies for Retirees

While RMDs are mandatory, retirees can use strategies to minimise their impact:

● Coordinate with tax brackets: Spread withdrawals and other income sources strategically to keep taxable income lower.

● Roth conversions: Moving funds from a traditional IRA to a Roth IRA before reaching RMD age can reduce future RMDs, since Roth IRAs don’t require withdrawals during the owner’s lifetime.

● Early withdrawals: Taking money out before the required age can smooth out income and help with budgeting.

Working with a financial advisor, such as those at RetireNova, can help you create a personalized retirement withdrawal strategy. A thoughtful plan may help you reduce RMD taxes, maintain steady income, and make the most of your retirement savings.

Conclusion

Understanding RMD rules is critical for anyone with a tax-deferred retirement account. The timing, calculation, and tax treatment of withdrawals can have a major impact on your overall financial plan. Missing a deadline or miscalculating an amount could lead to unnecessary penalties and higher taxes.

By learning the rules, using the right tables, and planning ahead, you can stay compliant and protect your retirement income. Trusted guidance from RetireNova can make this process easier, offering strategies that fit your individual needs and long-term goals.

FAQS

1. At what age do RMDs start?

RMDs begin at age 73 under current IRS rules. If you turned 72 in 2022 or earlier, your required withdrawals have already started.

2. What if I miss my RMD deadline?

Missing an RMD can lead to a 25% penalty on the amount not withdrawn, which may be reduced to 10% if corrected promptly.

3. Do Roth IRAs require RMDs?

Roth IRAs have no RMDs during the owner’s lifetime, but inherited Roth IRAs do require withdrawals based on IRS rules.

4. How do I calculate my RMD?

Divide your retirement account’s December 31 balance by the IRS life expectancy factor listed in the official RMD tables.

5. Can I withdraw more than the minimum?

Yes, you can always withdraw more than the required amount, but every dollar taken is taxable income in the year withdrawn.