Why Deadlines Matter in Retirement Planning

When it comes to retirement, how much you save is only half the story. The other half is when you save it. Every year, the IRS sets firm deadlines for when contributions must be made to count for that tax year. Miss those dates, and you could lose valuable tax benefits, employer matches, and even a year of potential investment growth.

Think of contribution timing as the rhythm of your retirement plan. A missed beat can throw off your progress, while consistent timing keeps your money compounding and your taxes lower. That’s why understanding and tracking your retirement contribution deadlines isn’t just smart, it’s essential.

At RetireNova, we believe good planning isn’t about chasing numbers; it’s about structure. Knowing your deadlines gives you the control and confidence to save on schedule, year after year.

Why Deadlines Are Important for Retirement Contributions

Deadlines may not sound exciting, but in retirement planning, they’re one of the easiest ways to gain (or lose) ground. The IRS sets these dates to define which tax year your contributions apply to, and that determines when your money starts working for you.

When you contribute to your 401(k) or IRA before the deadline, those dollars either reduce your taxable income (for traditional accounts) or start compounding tax-free (for Roth accounts). Wait too long, and you lose both opportunities: the tax advantage and an extra year of growth.

For example, if you forget to fund your IRA before April 15, 2026, that contribution no longer counts toward your 2025 taxes, meaning you’ll owe more in the current year and have less money growing for the future. Or if you delay your 401(k) contribution past December 31, you might also lose out on valuable employer matches, essentially leaving free money on the table.

In short, contribution deadlines aren’t just administrative dates. They’re part of your overall tax strategy, one that can save you thousands if managed correctly.

2025 Retirement Contribution Limits You Need to Know

Each year, the IRS adjusts retirement plan limits to keep pace with inflation, providing savers with a little more room to grow their nest eggs. For 2025, those limits have increased slightly, offering more opportunity to invest for your future.

Here are the key numbers to remember:

● 401(k), 403(b), and most 457 plans: up to $23,000 in employee contributions.

● Traditional and Roth IRAs: up to $7,500 in total contributions.

● Total 401(k) limit (including employer match): as high as $69,000.

These limits may look like numbers on a chart, but they represent your annual opportunity to build tax-advantaged wealth. Missing a year or even contributing less than you could can make a noticeable difference when you retire.

That’s why RetireNova encourages clients to plan early. Setting up automated contributions or quarterly check-ins keeps you on track and removes the stress of last-minute deadlines. The earlier your money goes in, the longer it can grow.

Maximum and Catch-Up Contributions in 2025

If you’re 50 or older, the IRS gives you one of the best savings advantages available: catch-up contributions. These extra allowances let you invest more each year to help close the gap before retirement.

For 2025, the limits are:

● 401(k) plans: an extra $7,500, bringing the total to $30,500.

● IRAs: an additional $1,000, raising the total to $8,500.

This might not sound like much, but it can make a meaningful difference. Contributing an extra $7,500 per year for just five years could add over $50,000 in retirement savings, and that’s before compounding.

The key is to start early. The sooner you make these contributions, the longer your money can grow tax-deferred. For late starters, catch-up contributions are more than a bonus; they’re a powerful tool to strengthen your retirement cushion.

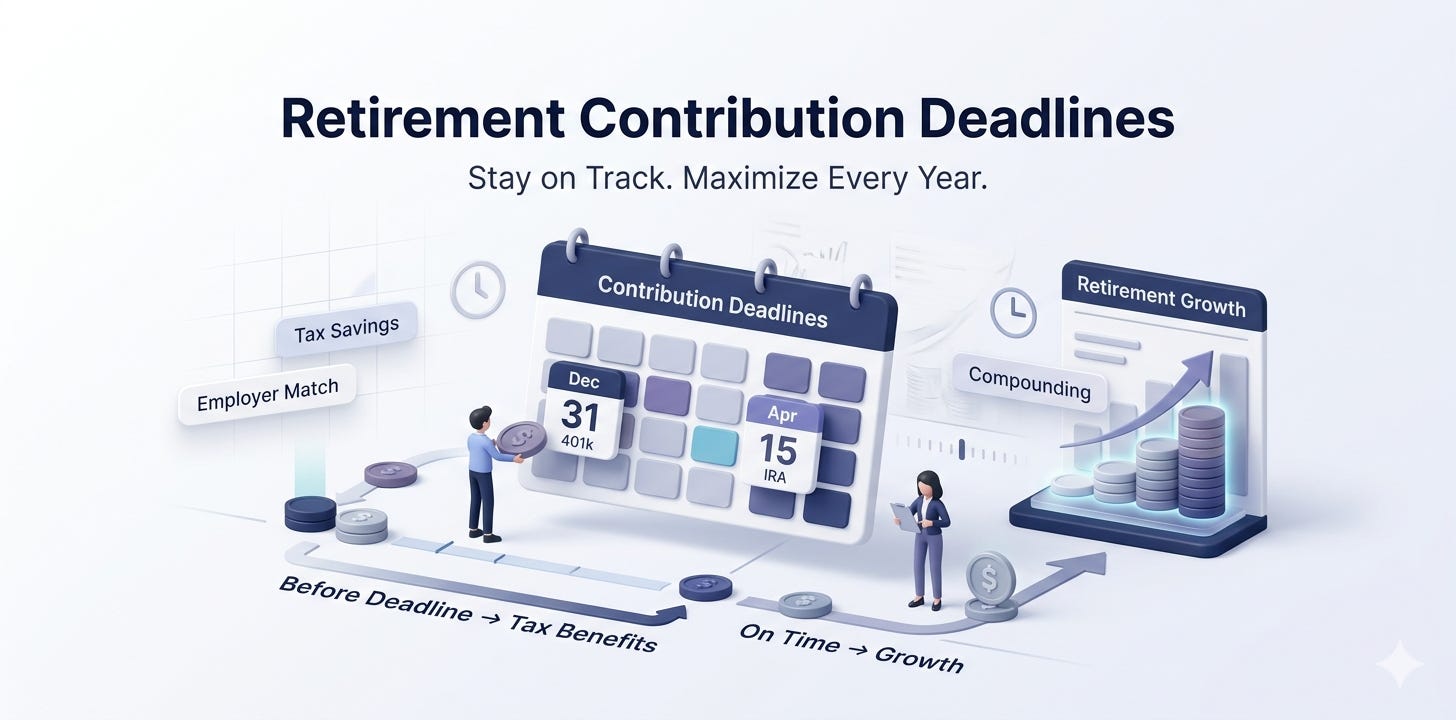

Key Retirement Contribution Deadlines by Account Type

Every retirement plan comes with its own rules and its own deadlines. Missing them can mean losing out on tax deductions or employer matches, so it’s crucial to understand the timeline for each account type.

Here’s a quick look at the 2025 contribution deadlines:

Account Contribution Deadlines for 2025 Tax Year

Traditional IRA / Roth IRA

Contribution Deadline: April 15, 2026 (Tax Day)

401(k), 403(b), 457

Contribution Deadline: December 31, 2025

SEP IRA (Self-Employed)

Contribution Deadline: Tax filing deadline, including extensions (up to October 15, 2026)

SIMPLE IRA

Contribution Deadline: Tax filing deadline, including extensions

Solo 401(k)

Employee: December 31, 2025

Employer: Tax filing deadline

What this means for you:

● Workplace plans like 401(k)s close at year-end, and there’s no grace period.

● Self-employed plans have more flexibility since they align with your tax filing schedule.

● Solo 401(k)s straddle both: you must make employee contributions by year-end, but employer contributions can wait until tax time.

Understanding these differences helps you prioritise where to save first and when.

Smart Strategies to Stay Ahead of Retirement

Contribution Deadlines

Even with the best intentions, life gets busy, and that’s when deadlines slip by. The good news? A few simple habits can help you stay on track without added stress.

Here’s how to stay ahead:

● Automate your contributions: Set up payroll deductions or automatic transfers from your bank to your retirement accounts.

● Use reminders: Add calendar alerts for mid-year and end-of-year check-ins.

● Spread out your contributions: Instead of waiting until April or December, make smaller deposits throughout the year to manage cash flow more easily.

● Stay consistent: A steady rhythm of contributions helps build discipline and reduces last-minute panic.

By treating contribution planning as part of your routine, not a once-a-year scramble, you’ll protect your tax advantages and keep your retirement savings on schedule.

How Deadlines Affect Your Tax Planning?

Retirement deadlines don’t just affect when you save; they can also impact how much you owe in taxes.

For traditional accounts like IRAs and 401(k)s, contributions made before the deadline can lower your taxable income for that year. For example, if you contribute the 2025 maximum of $23,000 to your 401(k) and fall in the 24% tax bracket, you could reduce your federal tax bill by roughly $5,000.

That’s real savings, and it compounds each year you stay consistent.

Roth accounts work differently. You don’t get an upfront deduction, but your withdrawals in retirement are completely tax-free. So whether you save pre-tax or post-tax, the key is timing: contributing before your deadlines ensures those benefits apply to the right tax year.

The smartest approach is to view your retirement contributions and your tax plan as one system. Aligning both gives you flexibility today and security later.

Common Mistakes People Make With Retirement Contribution Deadlines

Missing deadlines isn’t always about carelessness; it’s usually about timing and organization. But the cost can be real. Here are some of the most common missteps to watch for:

● Waiting until the last minute. Rushing in April or December can lead to missed transfers, errors, or insufficient funds.

● Assuming extensions apply to all accounts. Filing an extension for your taxes doesn’t automatically extend your IRA contribution window; those still close on April 15, 2026.

● Overlooking catch-up contributions. Many people over 50 forget to take advantage of the extra limits that could dramatically boost their savings.

● Not tracking contributions. Some people exceed annual limits and face IRS penalties, while others contribute less than they could and lose valuable growth time.

At RetireNova, we recommend setting up a monthly check-in for just 10 minutes to review contributions, deadlines, and balances. It’s a simple habit that can prevent costly mistakes and keep your plan on track year-round.

DIY Checklist: Stay Ahead of Retirement Contribution Deadlines

Here’s your quick-reference guide to keep your retirement savings plan running smoothly:

1. Know Your Deadlines. Mark December 31, 2025, for 401(k)s and April 15, 2026, for IRAs and Roth IRAs. Self-employed plans follow your tax filing date.

2. Automate Contributions. Set up payroll deductions or recurring bank transfers so you never miss a deadline or an employer match.

3. Use Catch-Up Options. If you’re 50 or older, add an extra $7,500 to your 401(k) or $1,000 to your IRA.

4. Track Limits and Adjust Early. Review 2025 contribution limits mid-year. Increase your savings if income or goals change.

5. Plan With Taxes. Coordinate contributions with your tax planning to maximise deductions and avoid last-minute surprises.

A few minutes of planning each month can save hours of stress and thousands in missed opportunities.

Stay Organized, Save More, Retire Confidently

Retirement success isn’t built on luck; it’s built on timing, consistency, and structure. When you know your contribution limits and meet your deadlines each year, you gain more than just tax benefits. You unlock a cycle of steady growth, reliable employer matches, and compounding that works quietly in your favour.

The earlier you start, the easier it becomes. Small, scheduled contributions and good record-keeping can make your future retirement feel predictable instead of stressful. At RetireNova, we believe peace of mind comes from clarity, knowing exactly where your money is going, when it’s invested, and how it’s helping you reach your goals.

Our advisors help clients stay on track with easy-to-follow plans that fit real life. Whether you’re just starting or catching up, structure and timing are the foundation of a confident retirement.

FAQs

A. Deadlines & Rules FAQs

1. What is the retirement contribution deadline for 2025?

For 401(k), 403(b), and 457 plans, the deadline is December 31, 2025. For IRAs and Roth IRAs, you have until April 15, 2026 (Tax Day) to make your contributions for the 2025 tax year.

2. Do self-employed retirement plans have different deadlines?

Yes. SEP IRAs and Solo 401(k) employer contributions follow your tax filing deadline, including extensions, usually October 15, 2026, if extended.

B. Contribution Limits & Catch-Up FAQs

3. What are the 2025 IRS retirement contribution limits?

For 2025, you can contribute up to $23,000 to a 401(k) or similar plan, and $7,500 to an IRA. Including employer matches, total 401(k) contributions can reach $69,000.

4. Can I make catch-up contributions if I’m over 50?

Absolutely. If you’re 50 or older, you can add an extra $7,500 to your 401(k) and $1,000 to your IRA, bringing your total potential savings to $30,500 and $8,500, respectively.

C. Missed Deadline & Penalty FAQs

5. What happens if I miss a contribution deadline?

If you miss the cutoff, your contribution won’t count for that tax year, meaning you lose out on deductions, compounding time, and any potential employer matches for that period.

6. Can I make late contributions after filing taxes?

Not for most accounts. Once the IRS deadline passes, you generally can’t retroactively add contributions. The only exception is for self-employed plans with extensions tied to your tax filing date.