When you claim Social Security is one of the most important retirement decisions you’ll make. Unlike your investments, Social Security provides a guaranteed income stream for life — and the age at which you start taking it can mean the difference of tens of thousands of dollars over your lifetime.

Claim too early, and your monthly benefit shrinks permanently. Wait too long, and you may miss years of payments you could have enjoyed. The right choice depends on your health, finances, and goals.

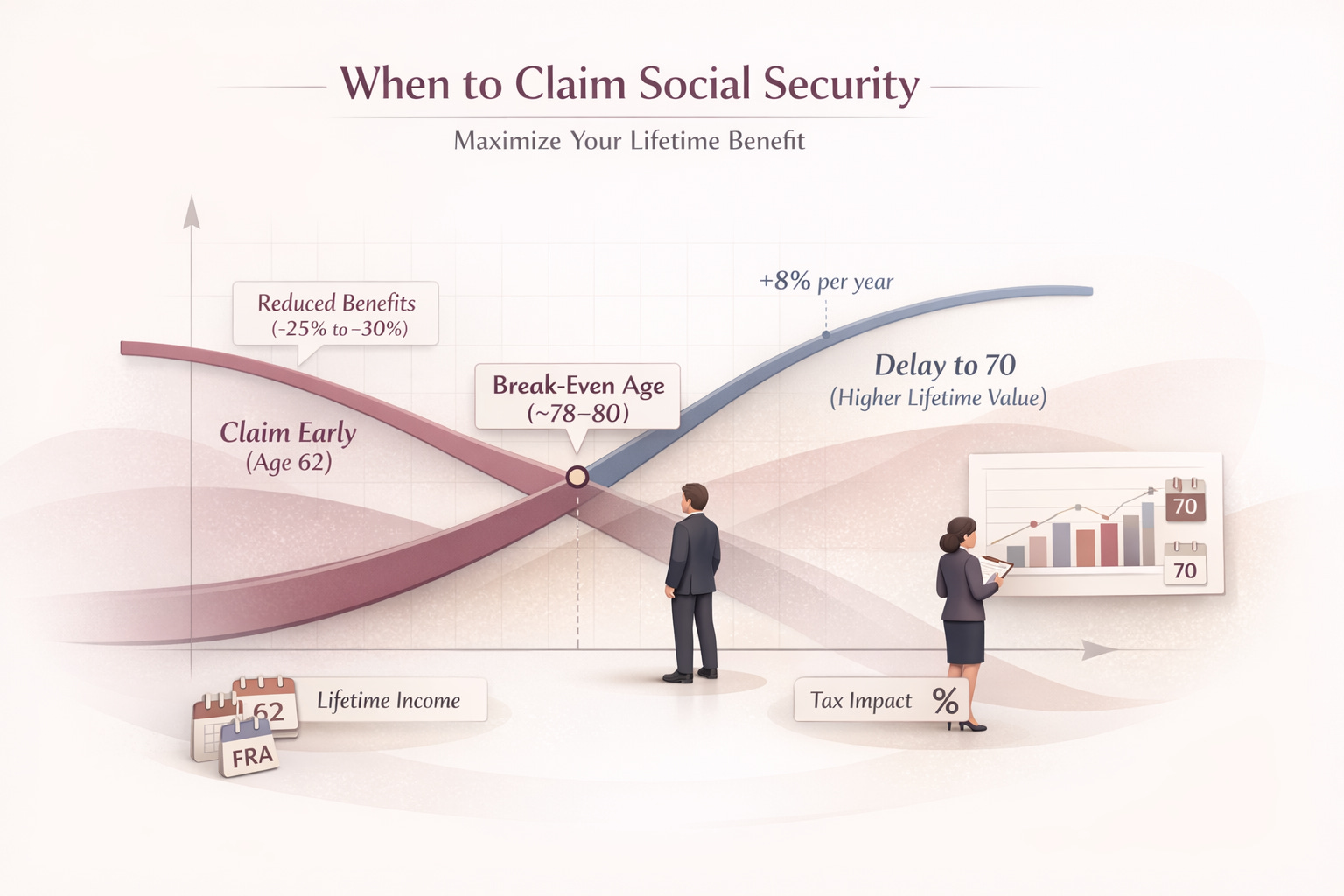

The Claiming Age Range: 62 to 70

● Earliest Possible Claim: Age 62

You can start benefits as early as 62, but they’ll be reduced by 25% to 30% compared to your full retirement age (FRA) amount. The reduction is permanent — you’ll never get the full benefit. Example: If your FRA benefit is $2,000/month, claiming at 62 could reduce it to around $1,400–$1,500/month.

● Full Retirement Age (FRA)

FRA is 66–67, depending on your birth year. At FRA, you get your full calculated benefit, with no reduction or increase.

● Latest Claim: Age 70

Waiting past FRA increases your benefit by 8% per year through “delayed retirement credits.” If your FRA is 67 and your benefit is $2,000/month, waiting until 70 could raise it to about $2,480/month — and you keep that higher amount for life.

Factors That Should Influence Your Timing

1. Life Expectancy & Health

● If you have serious health issues or a family history of shorter lifespans, claiming earlier may let you receive more total benefits.

● If you’re healthy and expect to live into your late 80s or beyond, delaying can be a better bet.

2. Need for Income

● If you’ve retired and need income to cover essentials, starting early may be unavoidable.

● If you can bridge the gap with savings, part-time work, or other income, delaying could increase long-term security.

3. Spousal Benefits

● Married couples can coordinate claiming to maximize household income.

● A higher-earning spouse may delay to boost survivor benefits for the lower earner.

● A lower-earning spouse may claim earlier to provide some income while the higher earner delays.

4. Taxes

● Up to 85% of your Social Security can be taxable, depending on your total income.

● Delaying may allow you to withdraw from IRAs at lower tax rates before benefits begin.

Break-Even Analysis: The Math Behind the Decision

A break-even age is the point at which the total money collected by delaying equals the amount you would have collected by starting earlier.

● For many, the break-even point is around age 78–80.

● If you expect to live well beyond that, delaying often pays off.

● If you may not reach it, starting earlier could make sense.

Special Strategies to Maximize Benefits

File and Suspend (No Longer Available in the Old Form)

● Before 2016, one spouse could file and suspend to let the other claim spousal benefits while both delayed their own — this loophole is mostly gone, but some older retirees still benefit.

Restricted Application

● If born before January 2, 1954, you may still be able to claim only spousal benefits while letting your own grow.

Survivor Benefit Timing

● Widows and widowers can claim survivor benefits as early as age 60 and later switch to their own benefit if it’s higher.

Practical Steps to Decide When to Claim

1. Get Your Social Security Statement — Create an account at SSA.gov to see your earnings history and estimated benefits at 62, FRA, and 70.

2. Run Multiple Scenarios — Consider different ages and calculate lifetime totals.

3. Incorporate Spousal Coordination — Look at combined lifetime benefits, not just one person’s.

4. Factor in Other Income Sources — If delaying Social Security lets you withdraw from retirement accounts at lower tax rates, it can be doubly beneficial.

Bottom Line:

The decision of when to claim Social Security is as much about longevity, taxes, and household needs as it is about the monthly amount. By running the numbers, weighing your health outlook, and coordinating with a spouse, you can make a choice that maximizes your lifetime income and security.