Social Security is often seen as the reliable pillar of retirement income — a steady check from the government that you can count on for life. But when you look closer, the timing of when you claim it, the taxes you’ll pay, and the penalties for starting too early can make a dramatic difference in the size of your benefit and the long-term security it provides.

Understanding these rules isn’t just about getting the most out of Social Security — it’s about fitting it into your overall retirement strategy, especially if you plan to stop working before the traditional retirement age.

How Social Security Benefits Are Calculated

Your benefit amount is based on your highest 35 years of earnings, adjusted for inflation. If you worked fewer than 35 years, the Social Security Administration (SSA) fills in the gaps with zeros, which lowers your average and reduces your benefit.

You can check your personalized estimate by creating a “my Social Security” account online. This estimate assumes you’ll keep working at your current income until the age you claim, so if you retire earlier, your actual benefit may be lower than what you see today.

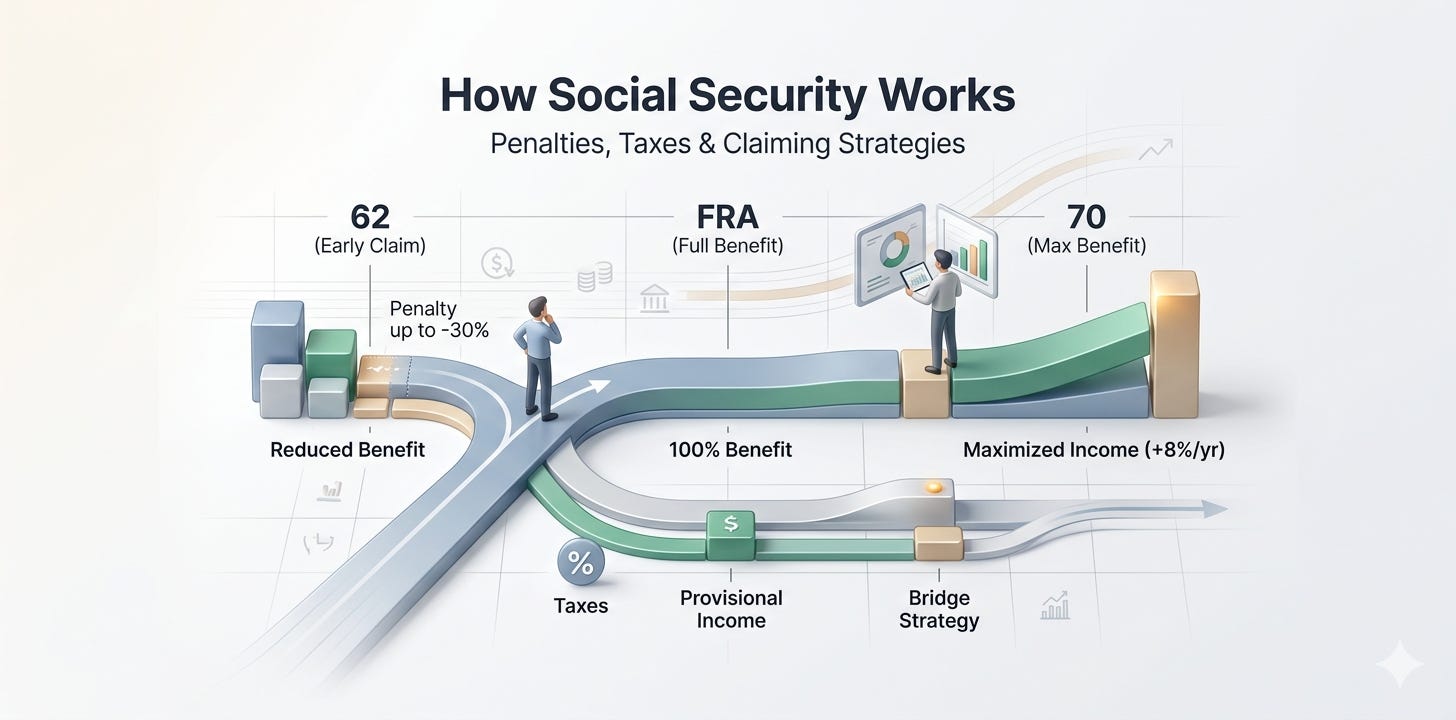

Key Ages to Know

● 62 — The earliest you can claim benefits. This comes with a permanent reduction of up to 30% compared to waiting until full retirement age (FRA).

● Full Retirement Age (FRA) — Between 66 and 67 depending on your birth year. Claiming at FRA gets you 100% of your calculated benefit.

● 70 — The latest age to start benefits. For every year you delay past FRA, you earn delayed retirement credits of about 8% per year, up to age 70.

The Penalty for Claiming Early

If your FRA is 67 and you claim at 62, you’re locking in a reduced benefit for the rest of your life. That means if your FRA benefit is $2,000 per month, claiming at 62 could reduce it to around $1,400 — a difference of $600 every month. Over a 20-year retirement, that’s well over $140,000 in lost income.

For early retirees, this creates a challenge: do you take a smaller check sooner to avoid draining other accounts, or do you bridge the gap with other savings so you can claim a larger benefit later?

Taxes on Social Security Benefits

Many people are surprised to learn that Social Security benefits can be taxable. The IRS looks at your provisional income — which includes half your Social Security plus all other taxable income and some tax-free interest.

● If you’re single and your provisional income is over $25,000, or married filing jointly over $32,000, up to 50% of your benefits may be taxable.

● If your provisional income exceeds $34,000 (single) or $44,000 (married), up to 85% of your benefits may be taxable.

This means your Social Security strategy can’t be separated from your withdrawal strategy — drawing heavily from tax-deferred accounts can push more of your benefits into the taxable range.

Claiming Strategies

There’s no one-size-fits-all answer, but some of the most effective strategies include:

● Delay if you can afford it — Waiting until 70 maximizes your monthly check, which is especially valuable if you expect a long retirement.

● Bridge with other income — Use savings, part-time work, or other accounts to cover expenses until you claim at a later age.

● Claim early if health is a concern — If you have reason to believe you won’t live into your 80s or 90s, starting earlier may make sense.

● Coordinate with a spouse — One spouse might delay to maximize survivor benefits while the other claims earlier to provide current income.

Why Social Security Is Part of the “Bridge Years” Puzzle

For those retiring before 62, Social Security is off the table for a while — which means the bridge years rely entirely on other sources of income. Even if you plan to retire at 62 exactly, you still face the trade-off between starting early at a reduced rate or waiting for a higher lifetime benefit.

The decision doesn’t just affect you — it can impact a surviving spouse’s income for decades.

Bottom line: Social Security is more than a government check. It’s a flexible, powerful piece of your retirement plan that requires thoughtful timing to maximize its value. For early retirees, the key is designing a bridge strategy that allows you to claim on your own terms — not out of necessity.

If you’re ready, I can now move into Post #7 – How Required Minimum Distributions (RMDs) Work: Penalties, Taxes, and Strategies to Reduce Their Impact, which is the final core piece of this early retirement planning series.