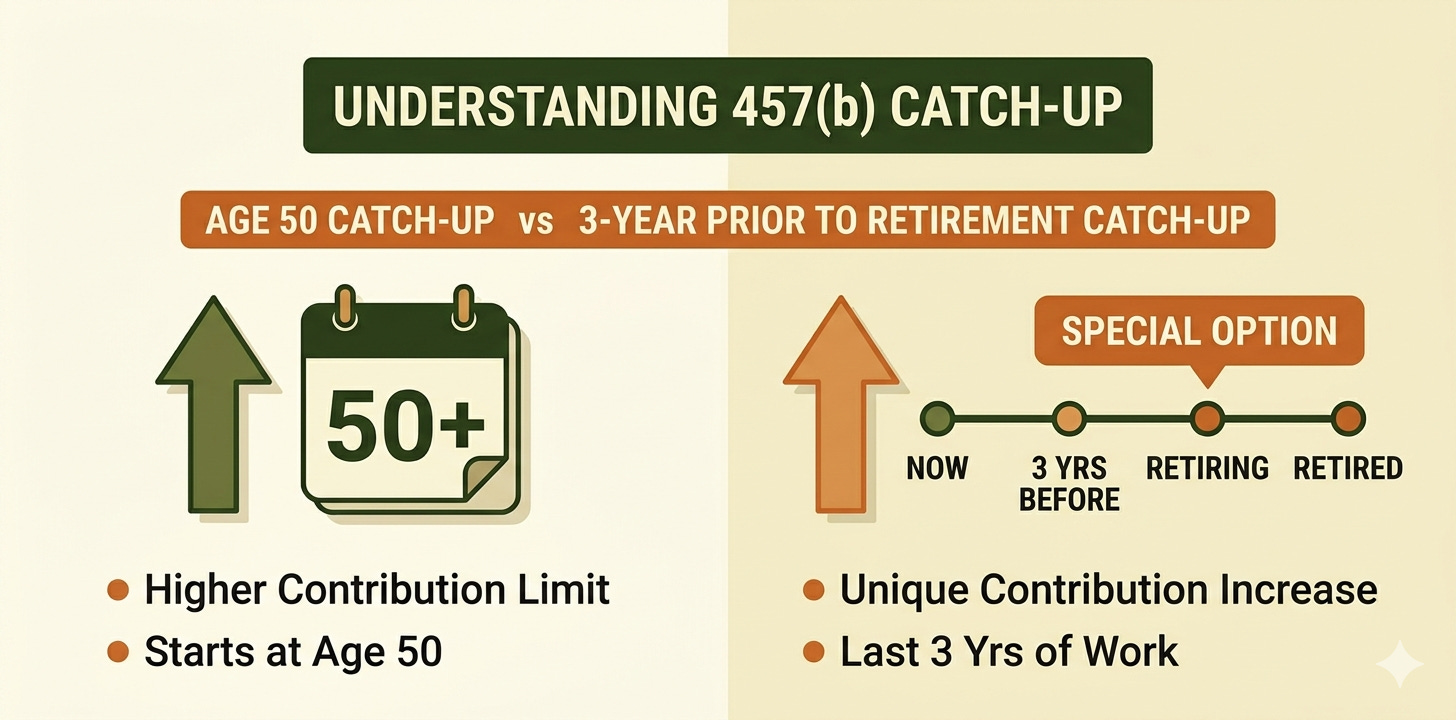

How Do Catch-Up Contributions Work in 457(b) Plans (Age 50 Catch-Up vs 3-Year Prior to Retirement Catch-Up)?

457(b) plans are designed to help public sector and non-profit employees build retirement savings with unique flexibility. One powerful feature is the catch-up contribution, which allows participants nearing retirement to save beyond the standard annual contribution limits.

In this article, we’ll explain:

How the age 50 catch-up works

How the special 3-year “final” catch-up works

Key differences between the two

How providers like T. Rowe Price apply these rules

Which strategy may work best depending on your retirement timeline

Standard 457(b) Contribution Limits

For 2025, the regular contribution limit for 457(b) plans is $23,000. This is the baseline amount employees can defer from their salary on a pre-tax or Roth basis.

Catch-up provisions allow eligible participants to go beyond this cap in certain circumstances, either due to age or proximity to retirement.

The Age 50 Catch-Up Rule

Who Qualifies?

Available to participants age 50 or older by the end of the calendar year.

Governmental 457(b) plans, including those managed by T. Rowe Price, typically allow this option.

Contribution Limit

Adds an extra $7,500 on top of the standard limit.

For 2025, eligible participants could contribute up to $30,500 ($23,000 + $7,500).

How It Works in Practice

If you’re 52 years old with a T. Rowe Price 457(b), you can elect to defer $30,500 for the year. This works just like the age 50 catch-up in 401(k) or 403(b) plans, giving older workers more opportunity to save in their peak earning years.

The 3-Year Prior to Retirement Catch-Up

Who Qualifies?

Available to participants who are within 3 years of the plan’s “normal retirement age” (defined by the plan, often between 65 and 70½).

This provision is unique to 457(b) plans and not available in 401(k)s or 403(b)s.

Contribution Limit

Participants may contribute up to twice the annual limit ($46,000 in 2025).

However, the actual catch-up amount is limited by unused contribution room from prior years.

How It Works in Practice

Suppose you’re 64 and plan to retire at 67. Your T. Rowe Price 457(b) records show that in past years you didn’t always contribute the maximum. Under the 3-year catch-up rule, you can “make up for lost time” by contributing beyond the standard limit, up to the lesser of:

$46,000 (2x the standard limit), or

The standard limit plus your unused contributions from earlier years.

This feature is especially valuable for late-career employees who couldn’t save the maximum earlier.

Key Differences Between the Two Catch-Up Rules

Feature Age 50 Catch-Up 3-Year Final Catch-Up

Eligibility: Age 50+ Within 3 years of plan’s normal retirement age

Extra Amount (2025): $7,500 Up to $23,000 (total limit $46,000)

Tied to Past Contributions?: No Yes, must have under-contributed in

prior years

Can Both Be Used Together?: No, participants must choose one in a given year

Plan Type: Governmental 457(b)s Governmental 457(b)s

How T. Rowe Price Applies These Rules

As a major 457(b) plan administrator, T. Rowe Price follows IRS guidelines closely:

Plan documents define the normal retirement age used for the 3-year catch-up.

T. Rowe Price tracks participant contribution history to calculate eligible unused amounts.

Participants must formally elect which catch-up provision they intend to use for the year.

The plan ensures IRS limits are not exceeded, preventing double use of both catch-ups.

Tax and Retirement Planning Implications

Accelerating Savings Near Retirement

The 3-year catch-up can allow massive contributions in your final working years.

Ideal for participants who expect lower expenses and higher disposable income close to retirement.

Flexibility of Age 50 Catch-Up

Simple and consistent—no need to calculate past under-contributions.

Good for those steadily maxing out savings after age 50.

Roth vs. Traditional Deferrals

Both catch-ups can be directed into either pre-tax or Roth contributions (if the plan allows).

Strategic choice depends on whether you expect higher or lower taxes in retirement.

Coordination with Other Plans

If you also participate in a 403(b) or 401(k), those limits are separate from the 457(b). This means you could potentially contribute much more overall.

Example Scenarios

Maria, Age 55 (Age 50 Catch-Up)

Maria participates in a T. Rowe Price 457(b) and earns enough to save aggressively. She contributes the maximum $30,500 in 2025, taking advantage of the age 50 catch-up every year until retirement.

James, Age 64 (3-Year Final Catch-Up)

James is three years from retirement age. Over his career, he often contributed below the limit. With the 3-year catch-up, he can defer up to $40,000–$46,000 annually, depending on his unused contribution room.

Both strategies work but which is best depends on your career stage and financial history.

About Nova Wealth

At Nova Wealth, we focus on helping retirees and pre-retirees build predictable and sustainable income in retirement. Our approach centers on personalized strategies that deliver steady, reliable cash flow so you can enjoy your next chapter with confidence. We believe retirement should feel secure and stress free free from uncertainty and full of clarity.

Whether you are evaluating 457(b) rollover options, considering catch-up contributions, or planning for emergency distributions, Nova Wealth is here to guide you every step of the way. Contact us today to start building a retirement income plan designed to give you peace of mind for the years ahead.