If you’ve been building your retirement savings through a T. Rowe Price 457(b) retirement plan, there will come a time when you consider moving your money into another retirement account. Whether you’re changing jobs, retiring, or consolidating your retirement plans, it’s important to understand the distribution rules, tax implications, and available investment options before making a decision.

This guide explains how a rollover works, when you can initiate it, and the benefits or drawbacks all within the framework of IRS rules for 457(b) plans.

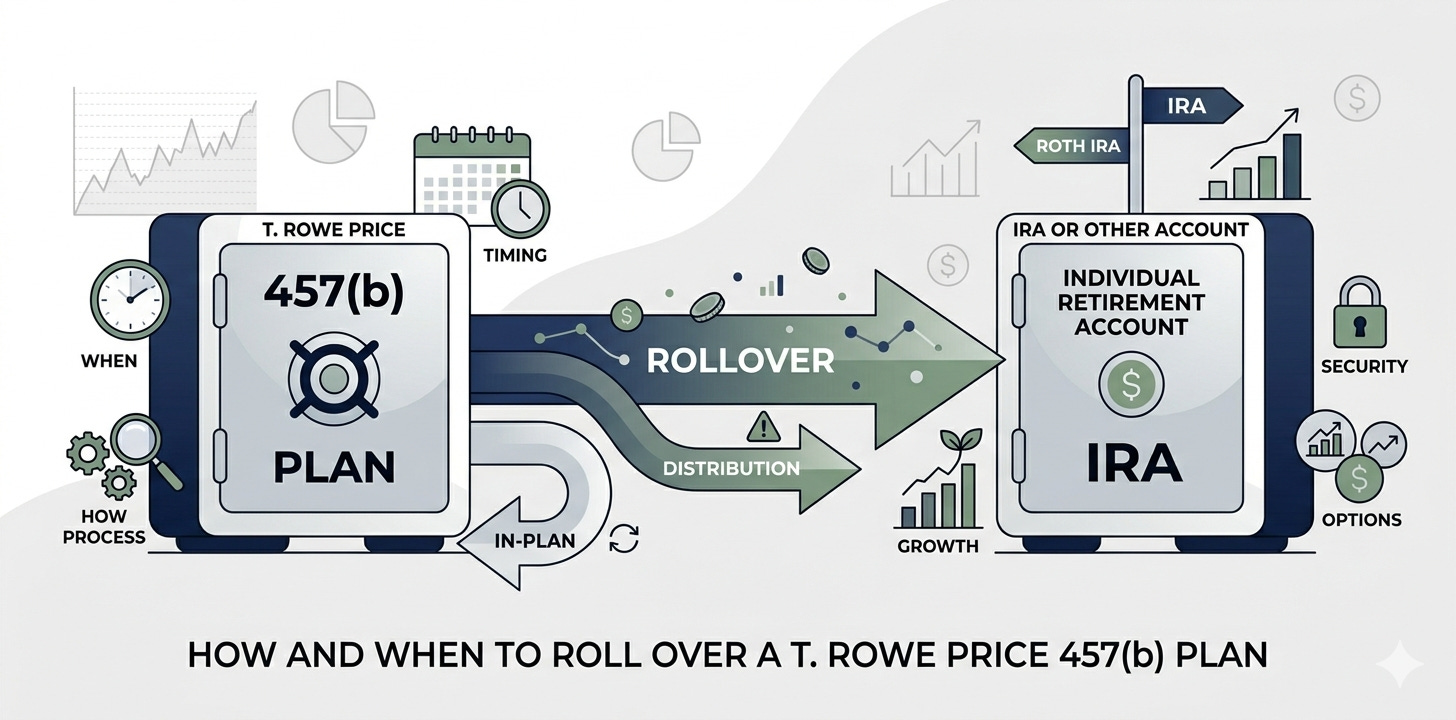

Understanding 457(b) Plans and Rollovers

A 457(b) Deferred Compensation Plan is a tax-advantaged retirement savings plan designed for public sector employees and certain non-profits. Contributions grow with tax deferral benefits, and withdrawals in retirement are taxed as ordinary income tax.

With T. Rowe Price, participants gain access to broad investment plan choices, such as Target Retirement Funds and even Vanguard ETF options. But many retirees eventually roll funds into IRAs or other qualified retirement plans for additional control, lower investment management fees, or access to broader financial planning tools.

Eligible Rollover Destinations

Funds from a governmental 457(b) plan can be moved into:

Traditional IRAs – Keep the tax-deferred structure and continue growing your account balance until Required Minimum Distributions (RMDs) begin.

Roth contributions into a Roth IRA – Pay income tax on the conversion now, but enjoy tax-free withdrawals later.

Another 401(k) plan or employer-sponsored retirement plan – Consolidate accounts under a new employer, as long as the plan administrator accepts rollovers.

This process is often completed through a trustee-to-trustee transfer, sometimes called a direct 457(b) rollover, which avoids penalties and preserves tax savings.

When Can You Roll Over a T. Rowe Price 457(b) Retirement Plan?

Job Change or Retirement

After leaving your employer, you can complete an account transfer to another IRA or qualified retirement plans.

In-Service Withdrawals

Some plans allow limited penalty-free withdrawals after age 59½, but you’ll need to check with your plan administrator about rollover restrictions.

At Retirement

Many retirees prefer rolling into IRAs for better control, reduced administrative fees, and broader investment options.

Tax Implications of Rollover Decisions

Direct Rollover (Trustee-to-Trustee Transfer): No taxes withheld, funds move seamlessly to another retirement account.

Indirect Rollover: You receive the money first, then have 60 days to deposit it. Beware of mandatory 20% federal income tax withholding if you choose this method.

Roth IRA Conversion: Rolling into a Roth requires paying income tax upfront, but it can maximize future retirement income with tax-free distributions.

Keep in mind: rolling from a governmental 457(b) plan into an IRA removes the unique benefit of penalty-free withdrawals before 59½.

Pros of Rolling Over

More Investment Options beyond what’s in your T. Rowe Price lineup.

Lower Costs if you avoid high investment management fees or hidden administrative fees.

Account Consolidation across different employer-sponsored retirement plans.

Better financial planning tools and estate planning flexibility.

Cons of Rolling Over

Loss of the special early withdrawal advantage unique to governmental 457(b) plans.

Roth conversions increase income tax in the year of transfer.

Possible loss of employer features, like loan provisions or access to certain company stock.

Example Scenarios

Case 1: Retiree at 62

Rolls over to a Traditional IRA. Keeps tax benefits, defers Required Minimum Distributions, and maintains control of their investment options.

Case 2: Mid-Career Employee at 45

Chooses a 401(k) plan rollover. Consolidates accounts but gives up penalty-free withdrawals available in a 457(b).

Final Thoughts

Rolling over a T. Rowe Price 457(b) retirement plan can unlock broader investment options, reduce costs, and simplify retirement planning. But it’s crucial to weigh the tax benefits, early withdrawal rules, and long-term impact on your retirement income. For many, working with a trusted financial advisor ensures the best outcome.

How Nova Wealth Can Help

At Nova Wealth, we specialize in helping retirees build smart, sustainable income plans. Whether you’re navigating 457(b) rollovers, planning for withdrawals, or figuring out what fits your retirement goals we’ll make sure you have clarity, confidence, and peace of mind. Contact Us today.