Retiring before age 65 can feel liberating — until you realize Medicare won’t start for years. Those “gap years” can be the most expensive for healthcare if you don’t plan carefully. Without employer coverage, you’re on the hook for premiums, deductibles, prescriptions, and unexpected medical bills. But with the right strategy, you can protect both your health and your wallet.

Step 1: Understand Your Healthcare Needs and Risks

● Review Your Medical History — If you have ongoing prescriptions, specialist visits, or chronic conditions, you’ll likely need a more comprehensive plan with lower out-of-pocket limits. That will cost more, but it may save thousands in care.

● Account for Family Coverage — Retiring early might also mean losing coverage for your spouse or dependents. Their health profiles should factor into the plan you choose.

● Project Future Costs — Use today’s quotes for your age and location, then add 5–8% annually to account for rising premiums. If a plan costs $900/month today, expect around $1,100/month in five years.

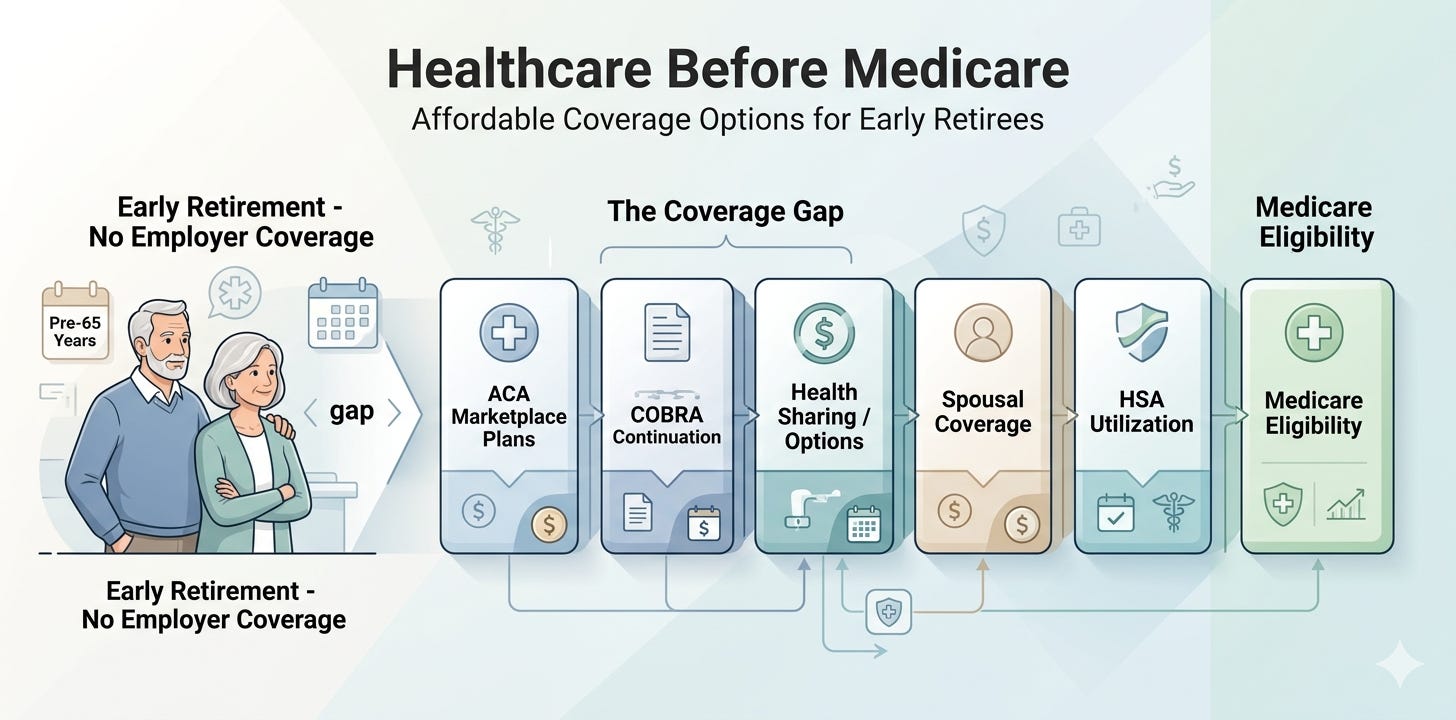

Step 2: Your Main Coverage Options

ACA Marketplace Plans (Healthcare.gov)

● Available nationwide, with premium subsidies based on your taxable income.

● If you control your income (by living off savings, Roth withdrawals, or low-tax assets), you may qualify for large subsidies — sometimes cutting premiums in half or more.

● Example: A couple with $50,000 taxable income might pay $600/month instead of $1,200/month for a Silver plan.

● Plans cover essential health benefits, and pre-existing conditions cannot be excluded.

COBRA

● Lets you continue your employer’s health plan for 18–36 months after leaving.

● You pay the full premium plus a 2% admin fee — often $800–$1,500/month for family coverage.

● Best if you only need coverage for a short bridge period or have complex medical needs your current plan already covers.

Spouse’s Employer Coverage

● If your spouse keeps working, joining their plan can be much cheaper than buying your own.

● Check whether adding you changes their employer’s contribution level.

Part-Time Work With Benefits

● Some employers offer health coverage to part-timers (e.g., Costco, UPS, Starbucks).

● This can be a way to earn income and get affordable insurance.

Health-Sharing Ministries

● Community-based cost-sharing arrangements, often lower-cost than insurance.

● Pros: Lower monthly costs. Cons: Not legally required to cover anything, often exclude pre-existing conditions, and may have restrictions on lifestyle or care types.

Step 3: Lower Premiums Through Tax Planning

● Withdraw From Roth IRAs/401(k)s — These withdrawals don’t count toward taxable income, helping you stay under ACA subsidy limits.

● Spend Cash Reserves First — Pull from savings or brokerage accounts before tapping traditional retirement accounts.

● Stagger Capital Gains — If you must sell investments, spread the sales over multiple years to avoid big spikes in income that kill your subsidies.

Step 4: Budget Beyond Premiums

● Deductibles — The amount you must pay before insurance kicks in. High-deductible plans have lower premiums but may cost more if you have frequent medical needs.

● Copays & Coinsurance — Fixed amounts or percentages you pay for doctor visits, prescriptions, and procedures.

● Out-of-Pocket Maximum — The cap on what you pay annually. A plan with a $7,500 out-of-pocket limit means that’s your worst-case scenario (excluding premiums).

Tip: Keep a “medical emergency fund” or sinking fund to handle deductibles and coinsurance without tapping investments at the wrong time.

Step 5: Max Out an HSA While You Can

● If you’re on a high-deductible health plan before retirement, contribute the annual maximum to a Health Savings Account (HSA).

● Contributions are tax-deductible, grow tax-free, and can be used tax-free for qualified medical expenses.

● After age 65, you can withdraw for any purpose (non-medical withdrawals are taxed, but no penalty).

● You can use HSA funds for COBRA premiums, ACA premiums, and all Medicare premiums except Medigap.

Step 6: Review Annually

● Marketplace premiums, subsidies, and plan designs change every year.

● During open enrollment, shop around even if you like your current plan — a competitor might offer better value.

● Adjust your tax strategy yearly to keep your income in the subsidy sweet spot.

Bottom Line:

If you’re retiring before 65, healthcare planning is as critical as investment planning. The wrong coverage choice can cost tens of thousands over your gap years. The right one can keep you protected and on budget — letting you enjoy your early retirement without fear of medical bills.

Healthcare Before Medicare: Affordable Coverage Options for Early Retirees

For many people, healthcare is the single biggest challenge in early retirement. Retiring before 65 means you won’t yet qualify for Medicare, leaving a potentially expensive coverage gap. Without a plan, those years between leaving your job and enrolling in Medicare can drain your savings fast.

The good news? You have multiple strategies to keep your healthcare affordable and reliable — if you plan ahead.

Step 1: Estimate Your Healthcare Needs and Costs

Start by understanding exactly what kind of coverage you’ll need.

● Know Your Medical History — If you have chronic conditions or ongoing prescriptions, factor in higher annual costs.

● Consider Family Coverage — If you have a spouse or dependents, their needs might dictate the type of plan you choose.

● Check Today’s Rates — Get quotes for various plans now, then adjust for projected annual premium increases of 5–8%.

Example: If a marketplace Silver plan is $800/month now, and you retire at 60, you’ll need to budget around $10,000–$12,000/year for premiums — plus out-of-pocket expenses.

Step 2: Explore Your Main Coverage Options

You likely have more options than you think:

1. ACA Marketplace Plans (Healthcare.gov)

● Available in every state, with subsidies based on income.

● If you keep taxable income low in retirement, you could qualify for significant premium reductions.

● Example: A couple with $50,000 in taxable income might pay half the full premium.

2. COBRA

● Lets you keep your employer’s plan for 18–36 months after leaving work.

● Usually the most expensive option because you pay the full premium plus a 2% admin fee.

● Works well as a short-term bridge if you retire just a year or two before Medicare.

3. Spouse’s Plan

● If your spouse is still working, you can join their employer coverage, often at a lower cost than buying your own plan.

4. Part-Time Work With Benefits

● Some companies, like Costco or UPS, offer health coverage to part-timers — a way to bridge the gap while earning extra income.

5. Health-Sharing Ministries

● These aren’t insurance, but rather cost-sharing arrangements among members.

● They can be cheaper, but they don’t guarantee payment and may exclude pre-existing conditions.

Step 3: Use Tax Planning to Lower Premiums

Since ACA subsidies are income-based, you can strategically keep taxable income low to qualify for savings.

● Withdraw From Roth Accounts — These withdrawals don’t count toward taxable income.

● Use Cash Reserves First — Spend down savings or taxable investments to avoid pushing income over subsidy thresholds.

● Time Capital Gains Carefully — Spreading investment sales over multiple years can keep your income in the subsidy-friendly range.

Step 4: Budget for Out-of-Pocket Costs

Premiums are just the beginning. You’ll also face:

● Deductibles — The amount you must pay before insurance starts covering costs.

● Copays & Coinsurance — The share you pay for doctor visits, prescriptions, and procedures.

● Out-of-Pocket Maximum — The most you’ll pay in a year before insurance covers 100% of costs.

Tip: Keep a dedicated “healthcare sinking fund” to cover these costs without dipping into long-term investments.

Step 5: Consider Health Savings Accounts (HSAs)

If you have an HSA-eligible high-deductible health plan before you retire:

● Contribute the maximum while working — contributions are tax-deductible, grow tax-free, and can be withdrawn tax-free for qualified expenses.

● After 65, HSA funds can be used for any purpose (though non-medical withdrawals are taxed).

● HSA dollars can be used to pay for premiums on certain plans, COBRA coverage, and all Medicare premiums except Medigap.

Step 6: Review Annually

Healthcare costs and rules change. Every year:

● Shop marketplace plans during open enrollment.

● Compare total costs — not just premiums — across options.

● Adjust your tax and income strategy to keep coverage affordable.

Bottom Line

Healthcare planning is just as important as investment planning when retiring early. By knowing your options, managing your taxable income, and budgeting for both premiums and out-of-pocket costs, you can confidently bridge the gap until Medicare kicks in.

A well-structured plan ensures your early retirement years are spent enjoying your freedom — not worrying about unexpected medical bills.