Social Security spousal benefits are an important part of retirement planning for many couples — especially when one spouse has a significantly higher earnings history or limited earnings. The goal is to coordinate benefit claiming so the couple maximizes lifetime income without leaving money on the table.

What Are Spousal Benefits?

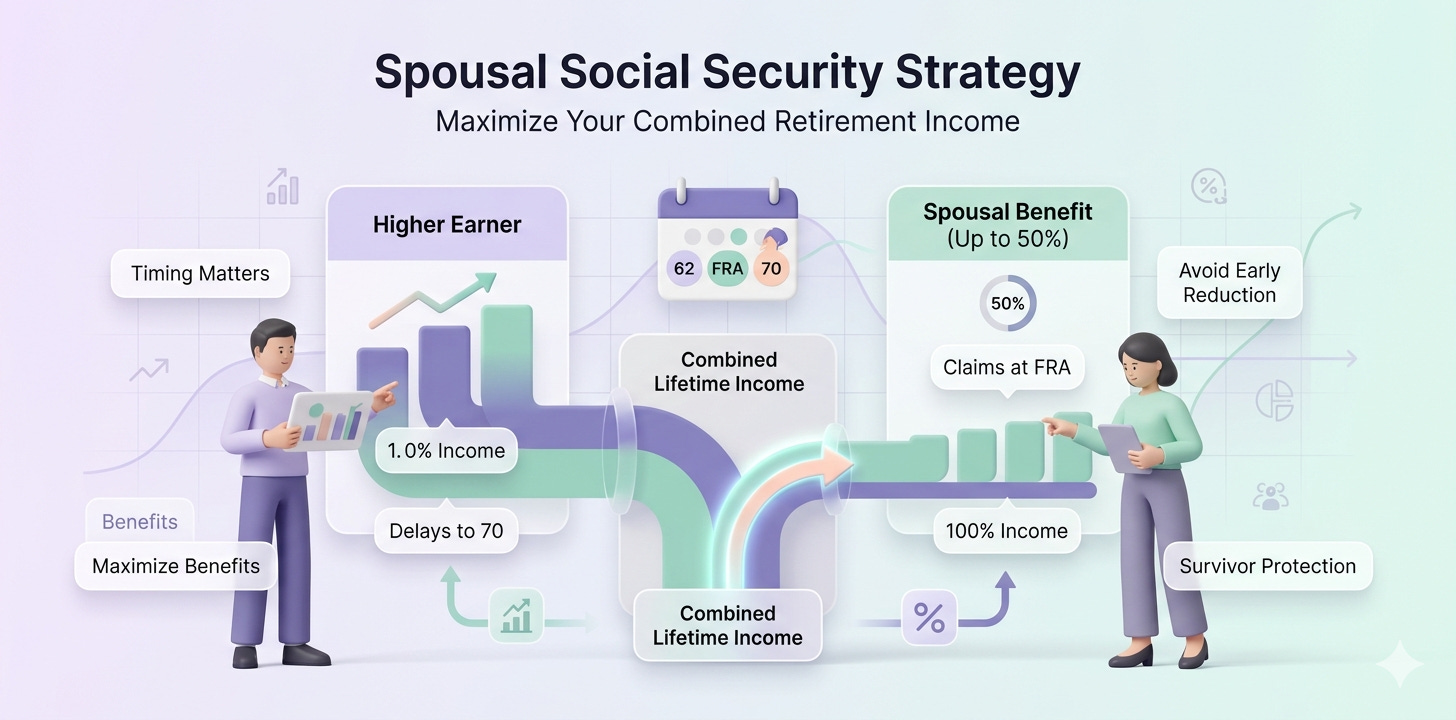

Spousal benefits allow a lower‑earning spouse to receive up to 50 % of the higher‑earning spouse’s Full Retirement Age (FRA) benefit, provided certain conditions are met. You receive either your own benefit or the spousal amount — whichever is greater.

Key Rules

1. Eligibility age: You must be at least 62 to begin spousal benefits (with reductions if taken before FRA). Encyclopedia Britannica

2. Marriage duration: You generally must have been married at least 1 year to qualify. Encyclopedia Britannica

3. Spouse must file first: The higher‑earning spouse must file for their own benefit before a spousal benefit can be paid.

4. No “double‑dip”: You don’t collect your own benefit plus half your spouse’s — Social Security pays the higher amount of the two. Encyclopedia Britannica

Timing Matters

● Claiming at Full Retirement Age (FRA): Up to 50 % of spouse’s PIA. Encyclopedia Britannica

● Claim before FRA: Benefits are permanently reduced based on how early you claim.

● Claim after FRA: Spousal benefits do not increase past FRA (unlike individual benefits). Forbes

Strategic Coordination

A thoughtful claiming strategy considers both spouses’ benefit amounts and ages. For instance:

● Let the higher‑earning spouse delay claiming to increase their benefit up to age 70. Forbes

● Have the lower‑earning spouse claim at or near FRA to capture the full spousal amount. This can increase lifetime benefits compared to both spouses claiming early.

Divorced Spouses

If you were married at least 10 years, you may qualify for spousal benefits on an ex‑spouse’s record even if you remarry — without reducing their benefit or affecting theirs. Encyclopedia Britannica

TACTICAL PLAN: Step‑by‑Step Guide

Step 1 — Estimate Benefits for Both Spouses

● Use the SSA estimator or “my Social Security” accounts to estimate each spouse’s benefit at ages 62, FRA, and 70. Kiplinger

● Determine each spouse’s Primary Insurance Amount (PIA) at FRA. Encyclopedia Britannica

Step 2 — Identify the Higher‑Earning Spouse’s PIA

● The spousal benefit is based on 50 % of the higher‑earning spouse’s FRA benefit. Encyclopedia Britannica

Step 3 — Compare Benefit Timing Scenarios

Model scenarios such as:

● Both spouses claim at age 62

● Lower‑earning spouse claims spousal benefit at FRA while higher‑earning spouse delays

● One spouse claims at FRA while the other delays to 70

This helps quantify total lifetime income and identify which combination maximizes benefits. Forbes

Step 4 — Consider Survivor Benefits

If one spouse dies first, the surviving spouse can often receive 100 % of the deceased spouse’s benefit (if larger). Plan claiming ahead to protect future income. Forbes

Step 5 — Account for Reductions

● Early claiming reduces monthly payouts permanently.

● Spousal benefits do not grow after FRA.

● Run multiple scenarios to see the tradeoffs and total lifetime value.

Step 6 — Coordinate with Taxes and Retirement Cash Flow Consider how claiming affects:

● Taxation of Social Security benefits

● Medicare premiums (IRMAA) based on income

● Income needs in early vs later retirement

Step 7 — Use Planning Tools

Enter your data into a professional retirement planner or SSA tools to test various claiming ages and outcomes before deciding.

TOP 10 FAQs (With Answers)

1. At what age can I claim spousal benefits?

You can start spousal benefits at age 62, but if you claim before your Full Retirement Age, the benefit is permanently reduced. Encyclopedia Britannica

2. Do I have to have worked to get spousal benefits?

No. Even if you have little or no work history, you can claim a spousal benefit based on your spouse’s earnings, provided you meet age and marriage requirements. Encyclopedia Britannica

3. Does my spouse have to be collecting Social Security before I can get spousal benefits?

Yes. The higher‑earning spouse must have filed for their benefit before the lower‑earning spouse can collect a spousal benefit.

4. Can I get my own benefit and a spousal benefit?

You won’t receive both separately. Social Security pays the higher of your own benefit or the spousal benefit — not both. Encyclopedia Britannica

5. How big can my spousal benefit be?

At Full Retirement Age, your spousal benefit can be up to 50 % of your spouse’s FRA benefit. Encyclopedia Britannica

6. Will my spousal benefit grow if I wait past FRA?

No. Unlike individual retirement benefits, spousal benefits do not increase if you delay past your FRA. Forbes

7. What about divorced spouses?

A divorced spouse may claim spousal benefits on an ex‑spouse’s record if the marriage lasted at least 10 years and you are currently unmarried. This does not reduce the ex‑spouse’s benefit. Encyclopedia Britannica

8. Does claiming early always reduce lifetime benefits?

Not necessarily — if you need the income sooner or have health/longevity considerations. But early claiming reduces monthly benefits permanently.

9. How does Social Security affect taxes?

Up to 85 % of benefits may be taxable depending on income. Claiming strategies can interact with other income and taxes — plan accordingly. Kiplinger

10. What’s the best claiming strategy for couples?

There’s no one “best” answer — it depends on relative earnings, health/longevity expectations, cash flow needs, and tax implications. Running multiple claiming scenarios helps you choose the strategy that maximizes combined lifetime income.