A 457(b) plan is a special type of retirement account, most often offered to state and local government employees, and sometimes to nonprofit workers. It’s similar to a 401(k) or 403(b), but with one big perk: you can often take money out penalty-free as soon as you leave your job.

In other words, you don’t have to wait until age 59½ like you would with other retirement plans. As long as the withdrawal qualifies as an “allowable distribution” under IRS and plan rules, you’ll avoid that extra 10% penalty tax.

Governmental vs. Non-Governmental 457(b) Plans

Governmental 457(b):

Offered by state/local government employers.

Funds are kept in a trust (safer).

Rollovers allowed to IRA, 401(k), or 403(b).

Roth contributions may be available.

Non-Governmental 457(b):

Offered by certain nonprofits to top employees.

Funds are employer assets (riskier).

Rollovers usually not allowed.

Roth contributions not permitted.

Allowable Distribution Events

You can take money out of a 457(b) plan penalty-free under these conditions:

Separation from Service

Retire, resign, or leave your job → withdrawals allowed immediately.

No age 59½ rule like 401(k)/403(b).

Reaching Retirement Age

Once you hit the plan’s defined “normal retirement age,” distributions are allowed.

Governmental plans often use 65–70½.

Plan Termination

If your employer ends the plan, accounts are distributed.

Death

Beneficiaries can receive distributions penalty-free.

Unforeseeable Emergency

Severe medical, accident, disaster, or funeral expenses.

Must be beyond your control.

Ordinary debt or planned expenses don’t qualify.

Small Balance Rule

Some plans allow immediate distribution if your balance is under $5,000.

Court Orders (QDROs)

Divorce settlements may trigger a court-ordered distribution.

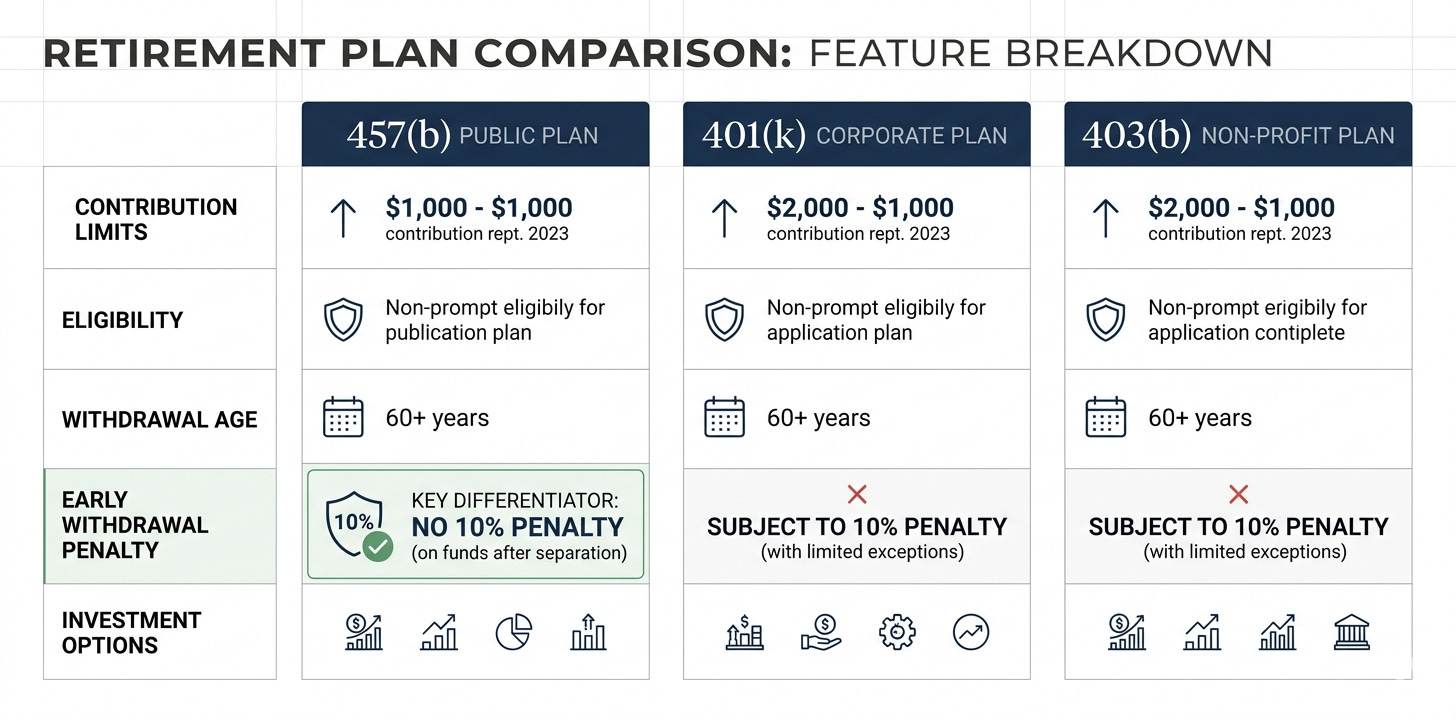

Why No 10% Penalty?

The IRS clearly states: 457(b) plan withdrawals are not subject to the 10% early withdrawal penalty.

This rule applies whether you are 40, 50, or 60 – age does not matter.

Regular income tax still applies to pre-tax contributions and earnings.

Key Differences from 401(k) & 403(b)

401(k)/403(b): Early withdrawals before 59½ usually face a 10% penalty.

457(b): Withdrawals after leaving your job have no penalty at any age.

Hardship vs. Emergency:

401(k)/403(b) allow “hardship withdrawals” (tuition, home purchase, etc.).

457(b) only allows “unforeseeable emergencies” (stricter).

Roth Contributions:

Governmental 457(b) may allow Roth (tax-free qualified withdrawals).

Non-governmental 457(b) does not.

Rollovers

Governmental 457(b) → rollover allowed to IRA, 401(k), 403(b).

Non-governmental 457(b) → no rollover option.

Tax Treatment of Withdrawals

Pre-Tax Contributions:

Taxed as ordinary income when withdrawn.

Roth Contributions (if available):

Withdrawals are tax-free if the account is at least 5 years old and you are 59½, disabled, or deceased.

If not qualified, earnings are taxed – but no penalty.

Required Minimum Distributions (RMDs)

RMDs must start at age 73 (or retirement, if later).

Failure to take RMDs = 50% IRS penalty on the missed amount.

About Nova Wealth

At Nova Wealth, we focus on helping retirees and pre-retirees build predictable and sustainable income in retirement. Our approach centers on personalized strategies that deliver steady, reliable cash flow so you can enjoy your next chapter with confidence. We believe retirement should feel secure and stress free free from uncertainty and full of clarity.

Whether you are evaluating 457(b) rollover options, considering catch-up contributions, or planning for emergency distributions, Nova Wealth is here to guide you every step of the way. Contact us today to start building a retirement income plan designed to give you peace of mind for the years ahead.